Contents

Key Insights

Maple Finance has limited potential in the lending service industry due to its current structure. Maple Finance lacks a major competitive advantage or valuation advantage over TrueFi, its primary competitor.

Business Overview

The major business of Maple Finance is credit lending/institutional credit lending. There are three roles in its process: borrowers, liquidity providers, and Pool Delegates.

Borrowers are cryptocurrency-native institutions, including market makers and market-neutral funds, who can lend money in an under-collateralized way, with a collateral rate ranging from 0-50%. Additionally, the main value proposition of Maple Finance is also to lend money to institutions on credit.

The liquidity provider (the lender; we will use the term “funding provider” below to avoid confusion) deposits funds into the liquidity pool to earn interest. The funding provider can claim the interest they earn at any time but withdraw the principal only after the loan is completed, and the withdrawal time is currently set at 180 days.

Liquidity Pool Delegates (also known as Pool Delegates) manage the liquidity pool in a capacity akin to that of a fund administrator. They must review the loan terms (the amount, term, interest rate, and collateralization rate), as well as the creditworthiness of institutional borrowers. A minimum of $100,000 in USDC-MPL(Maple’s native token) LPs must also be staked by Pool Delegates to the liquidity pool as loan collateral, with the money going back to the funders in the event of loan default.

In addition to the interest paid to the funders, the agreement will generate the fees as follows:

- The Establishment Fee

The Establishment Fee is equivalent to the financing service fee and is deducted directly at the lending time. The Establishment Fee is shared between Pool Delegates and the Maple Treasury, which periodically allocates it to all MPL holders.

- The Ongoing Fee

Ongoing Fees are paid for the ongoing management of each Lending Pool. They are set by the Pool Delegate and are paid out of a percentage of the interest yield received. The Ongoing Fee is shared between the Pool Delegate and MPL-USDC LP token stakers.

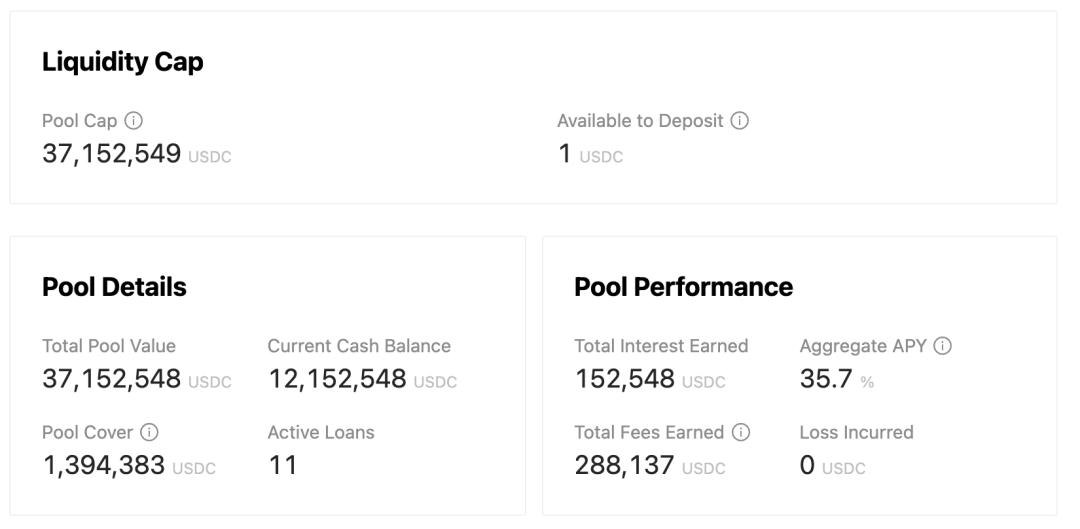

The first and only pool currently is the digital asset fund Orthogonal Trading, with Pool Delegates Josh Green, founder and CIO of Orthogonal Trading. The pool successfully lent $17 million on May 25 to borrowers, including Alameda Research, Wintermute, Amber Group and Framework Labs. At the end of June, the pool released a second tranche, bringing the total amount of funding to $37 million. The pool’s specifics are as follows:

Data Source: https://app.maple.finance/#/liquidity/60a48265ec0b150011480d2a

Basic Project Information

The Team

Founder Sidney Powell previously worked at Angle Finance, a non-bank lender in Australia, and before that, he was in National Australia Bank and was responsible for the institutional business. With the CFA certificate, Powell was a very early participant in DeFi and started exploring the possibility of DeFi non-hyper-collateralized lending in June ’19.

Joe Flanaga, the other co-founder, previously worked as a CFO for a listed company in Australia and had experience working for PWC.

According to LinkedIn, Maple Finance has 38 employees.

Overall, the founding team of Maple Finance has rich experience in traditional finance. At the same time, when compared to projects of the same size, the Maple Finance team gets more employees, and the team’s ability is somewhat stronger.

Milestones and Roadmap

Maple Finance initiated Maple Smart Bonds in the first place, a platform that enables users to do ABS on cDai (Certificate of Dai deposited in Compound), with 3-layer structure support. The first layer has better security (high collateralization rate) and slightly lower yield, the second layer has a slightly lower collateralization rate and higher yield, and the issuer should be the posterior layer. The product then had an MVP (minimum viable product), which also went live successfully in late 2019. It was a simulation of an ABS product in traditional finance, which did have the opportunity for development when cDai usage scenarios were insufficient. Still, the system would seem unnecessarily complex once available platforms support cDai collateral (e.g., Cream).

At the beginning of 2020, Maple officially transformed the business toward credit lending. They included the following when referring to the idea of lending as a simulation of Internet P2P business:

- Hawk: The collateral requirement is 0%, which is a full credit facility. But it thoroughly assesses new members by requiring copies of passports and zoom calls before adding them. Borrowers provide two payslips to show income. Targets medium size loans for cars or laptops. Interest is generally 5–9% for 18 months.

- Happy Medium: Higher 20% collateral requirement but new members only need to verify a LinkedIn or Twitter using Bloom. No payslips are required but Borrower addresses have to show they had at least 1,000 DAI in their address in the last 3 months, APR is generally 10–15% for 6–12 months.

- Light Touch: High 33% collateral, no identity validation required, uses an algorithm to assess the probability of default based on address tx history, small loans of less than 100 DAI, high APR of 40–50%.

In June 2020, they officially launched their front end with the same idea of Internet P2P. The noteworthy highlight is that they have partnered with an institution to launch a tx address-specific scoring system to replace the scorecard in traditional credit.

However, the simulation of offline P2P credit cannot solve the core problem: KYC of P2P loans and KYC-related credit (Fico score in the US and Credit in PBC) are scarce resources, while the addresses of on-chain loans are not. Only when the addresses are effectively linked to KYC (e.g., through tools such as BrightID) and the on-chain credit information can effectively help establish a perfect “recourse-as-a-service” in the real-world business. Otherwise, on-chain P2P credit will remain a niche market.

Their financing article disclosed a change in its business direction to institutional-oriented credit in December 2020, and in April, they announced the completion of the transformation.

Following the completion of the LBP (Liquidity Bootstrapping Pool) at the beginning of May this year, MapleFinance released its roadmap, which is now on track and fully implemented, including the following:

- On May 2, the project opened the 50:50 balancer pool – Upon completion of the Maple LBP, a 50:50 MPL: USDC balancer pool was created to provide initial secondary market liquidity for MPL tokens and serve as collateral to the start-up pool when the protocol is deployed. The initial MPL: USDC in the balancer pool is provided by MapleDAO Treasury and will be further supported by investors who will stake their MPLs in the first pool deployed on Maple.

- On May 12, The Maple protocol went live on the Ethereum mainnet and created its first liquidity pool. Orthogonal trading was launched as the first pool delegate to manage the initial $15M liquidity pool.

- On May 20, the project announced liquidity mining for consumers, where retail participants can deposit USDCs into the liquidity pool with a six-month lock period to receive USDC returns and MPL rewards.

- On May 25, the project reached $17 million in loans to borrowers (including Alameda Research, Wintermute, Amber Group and Framework Labs).

- The project launched the second liquidity pool and additional loans from late June to early July. The second pool of loans would be funded by Orthogonal Trading after four to six weeks following the start-up pool, and a second liquidity pool would be added to Maple. Borrowers placed on the waitlist will have the opportunity to submit loan applications.

- From the overview of Maple’s development history, they have been committed to the liquidity release of DeFi lending. Whether their first choice of asset securitization, P2P credit, or the current institutional lending is all focused on this direction, it is commendable that the team has been persistent in exploring and developing in this space.

The Financing

With a relatively strong group of investors, Maple Finance has raised money in two rounds.

Maple Finance, a DeFi lending platform for institutions and corporates, announced the closing of a $1.3 million seed round through the sale of governance tokens, MPL, from Cluster Capital, Framework Ventures, Alameda Research, FBG Ventures, One Block Capital, The LAO, Bitscale Capital, Synthetix founder Kain Warwick and Aave founder Stani Kulechov.

As of March 2021: valued at 5U/MPL (fully diluted market cap is $50 million)

Maple Finance closed a $1.4 million funding round led by Framework Ventures and Polychain Capital to help further develop and launch the pool.

According to the project’s disclosure in LBP, the valuation of this round was 5U/MPL, which means that the $1.4 million funding received a total of 280,000 MPLs. Based on the total 2.6 million MPLs received by the investors, we can deduce that the $1.3 million funding in the first round received a total of 2.32 million MPLs (2.6 million-0.28 million=2.32 million) at the end of 2020, and the cost of this round was 0.56U/MPL. We can find that the valuation of the first and second rounds went up nearly 10 times within 3 months.

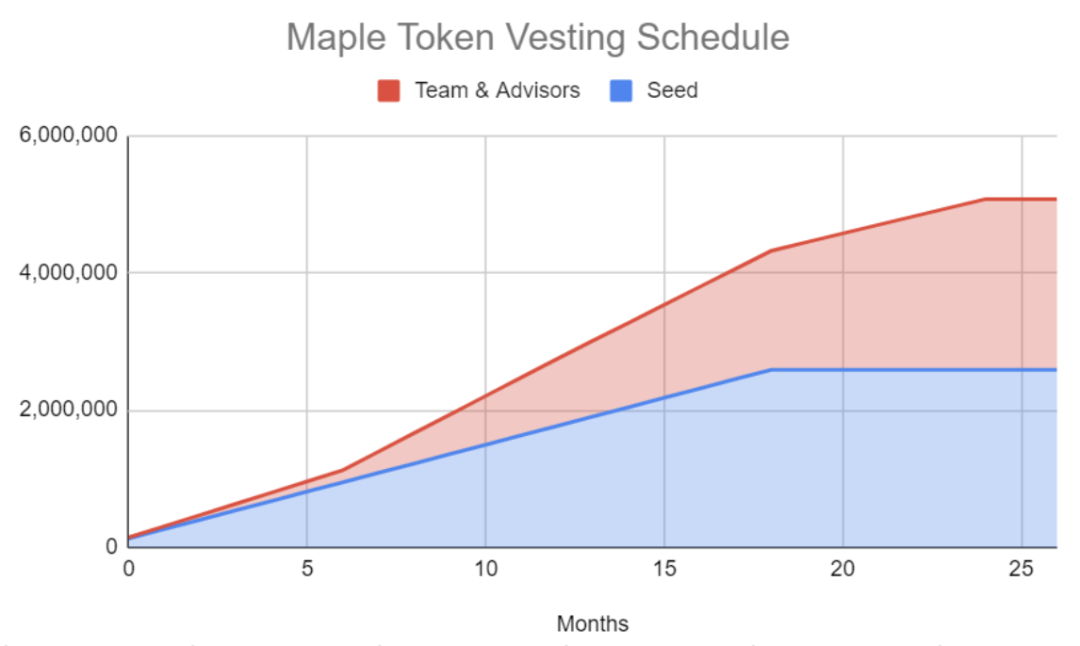

In addition, we also find that the team’s token has a 2-years vesting period, and the investor’s token has a 1.5-years vesting period.

Maple Finance successfully raised $10,332,236 through its LBP (Liquidity Bootstrapping Pool) on Balancer at the end of April 2021. The average cost of the LBP was $21.98, equivalent to an FDV of 220 million USDT.

Tokennomics

Token

MPL is the governance token of the protocol and has a max supply of 10,000,000. The token distribution and vesting structure look as follows:

Source: Maple Finance

Token Economy

In addition to governance, MPL can provide two other utilities—— sharing fees generated by the protocol and serving as the risk reserves which has not yet been launched.

As stated previously, MPL can share part of the establishment fee (distributed monthly by MPL, but the concrete proposal has not been mentioned) and a portion of the ongoing fee (by providing liquidity for risk reserves).

According to the official documentation, MPL-USDC LP is chosen to be the risk reserve. The Pool Delegate must prepare some risk reserves as a credit enhancement measure for the liquidity pool before creating it.

Price Trend

Data Source: CoinGecko

The current price of MPL is 6.37U, which is approaching the second round of the private sale.

The market capitalization of MPL is $10,200,000 million and its fully diluted valuation is $63,700,000.

Business Analysis

The Rivals

TrueFi is an obvious rival to Maple Finance’s institutional lending (non-flash loan) industry.

Maple and TrueFi are quite similar in that both are non-fully collateralized institutional lending platforms and neither offers a return of about 10% on stablecoins, with the majority of APY coming from distributions of their native tokens.

As a result, the Pool Delegate is utilized by Maple to introduce and assess loans, and a separate Pool Delegate can manage each lending pool. Each Pool Delegate resembles a fund manager in some ways and investors can choose from a variety of fund managers. Instead, all of TrueFi’s loans are evaluated by DAO, and investors who invest in TrueFi should have complete faith in the DAO’s investment capabilities. There is a major difference between the two, but we reckon it is the most important factor in business.

In terms of business data, after going live in late November 2020 and has been retweeted by SBF and AC, TrueFi has closed $220 million loans for institutions and acquired a number of institutional clients, including Alameda, Wintermute, and Poloniex.

Note: Alameda and Wintermute are clients of both Maple and TrueFi.

TrustToken, TrueFi’s operations team, closed a $20 million strategic funding round in 2018 led by a16z crypto, BlockTower Capital, Danhua Capital, Signia Venture Partners, Slow Ventures, and ZhenFund, all of which have fairly solid experience.

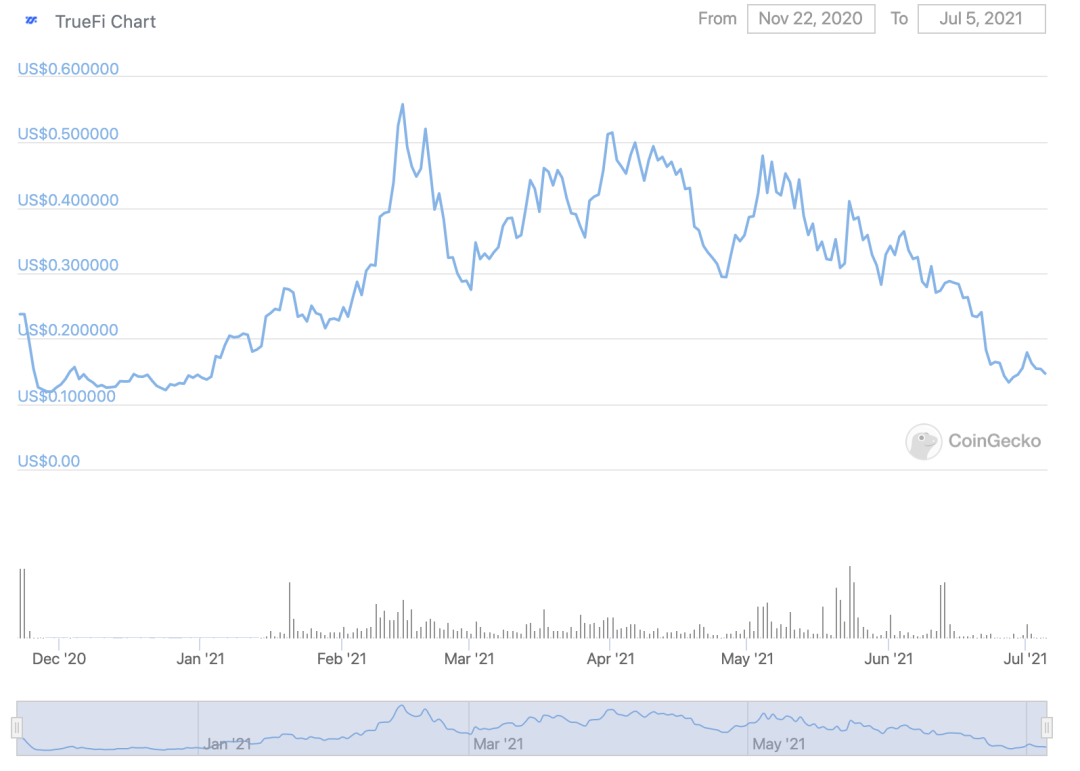

Already listed on Binance, $TRU has a circulating market cap of $51.15 million and a fully diluted valuation of $211 million. The token price is approaching its all-time low, with the price trend as the chart shows:

Source: CoinGecko

Goldfinch is another credit protocol and created by two former Coinbase employees, it has received $1 million in seed funding from Coinbase Venture and $11 million in Series A funding led by a16z. It has granted $1 million in loans to thousands of borrowers in Mexico, Nigeria, and Southeast Asia since its launch in December 2013. However, Goldfinch is focused on non-collateralized lending to individual borrowers, which is not quite in line with Maple Finance’s strategy.

The entire institutional lending industry is in its infancy at present. Maple does not demonstrate any substantial benefits over TrueFi in terms of business model, investors, business performance, or even market cap because the trading volume is still too small to be effectively valued.

Industry Analysis

The business direction of institutional lending Maple chose, on the one hand, is geared towards institutions, on the other hand, introducing new liquidity to non-collateralized lending by expanding credit leverage. These are the two segments of the market that we are optimistic about, but it seems not promising in terms of Maple’s current business.

If we describe Compound and Aave’s service to institutions as “introducing non-crypto institution money into the crypto market,” we can say Maple and TrueFi’s institutional lending service is “raising retail investors’ money to crypto institutions”. The extremely high risk-free yield rate in crypto (which is likely why Compound and Aave’s institutional business is preferred) and the limited yield rates institutions can pay are the fundamental drivers behind the tricky business of Maple and TrueFi.

According to TrueFi and Maple’s data, even for crypto institutions, the affordable loan rates range from roughly 8-10% for a 1-month term, 9-12% for a 3-month term, and 10-15% for a 6-month term. Due to business needs, deposits can only be fixed-term, meaning that users should give up the most crucial thing in crypto – liquidity. The loss of liquidity makes the yield seem not attractive enough, so Maple and TrueFi usually offer the project’s tokens as high incentives to funders to attract users.

On the one hand, it is not easy to maintain a high APY (i.e., token price); more importantly, after the distribution of project tokens, how to match the interest rate that institutions are willing to pay with the yield that retail investors can accept? That is the problem.

Institutions will be more rational, so the interest rates paid by borrowers will have a greater correlation with qualifications. The institutions willing to pay higher rates will be less qualified and thus riskier. And even for the top crypto institutions, their business is not absolutely safe (think of the hack attack and loss of Mentor and FireBlocks). For projects engaged in the institutional lending service, a single accident could seriously impact the project.

Overall, we reckon that institutional lending services will hit a plateau for now.

Reference

Coindesk:https://www.coindesk.com/maple-finance-corporate-lending-defi

Coindesk:https://www.coindesk.com/maple-finance-raises-1-4m-for-its-reputation-based-defi-lending-platform

Chiannews:https://chainnews-archive.org/posts/570022485536/

Maple Finance: https://app.maple.finance/#/liquidity

Maple gitbook: https://maplefinance.gitbook.io/maple/

Maple gitbook: https://maplefinance.ghost.io/guide-to-the-maple-lbp/

Medium: https://medium.com/swlh/crypto-lending-the-missing-ingredient-4862d54cdf53