Report Data as of: August 24, 2025

Contents

1. Research Summary

As a leading global crypto asset exchange and service provider, Coinbase leverages its brand trust, extensive user base, diversified product offerings, and early compliance initiatives to position itself as a core player capturing the long-term growth potential of the crypto industry.

Specifically:

- It has a long-standing track record and brand recognition in compliant operations and secure, reliable services, with numerous institutional partners, which helps attract both institutional and retail clients.

- Revenue from subscriptions, interest, and other sources is growing well, making the business model more diversified and less reliant on transaction fees, thereby enhancing its resilience to market cycles.

- The balance sheet is strong, with low leverage and ample cash on hand, providing the company with both a buffer and firepower for technological innovation, international expansion, and navigating challenging market conditions.

- In sovereign countries like the U.S., overall crypto regulations tend to be relatively permissive and innovation-friendly. The long-term industry trend still points to growth, with blockchain and digital assets expected to become increasingly integrated into mainstream finance. Coinbase has established strategic positions across key sectors of the industry.

However, while Coinbase’s revenue and profits have shown somewhat reduced volatility compared with the previous cycle, they still experience significant swings (see Section 6: Operations & Financial Performance). This has become particularly evident in the latest two quarters.

In addition, Coinbase operates in a highly competitive landscape. In the U.S., it faces direct competition from Robinhood and Kraken, while internationally, it contends with numerous offshore crypto exchanges such as Binance, rapidly growing decentralized exchanges like Uniswap, and on-chain platforms like Hyperliquid, all of which are challenging the market share of traditional centralized exchanges.

Notably, during this bull market cycle, Coinbase’s price rose over 11x from its 2022 low, far exceeding Bitcoin’s gains over the same period and outperforming the majority of crypto assets.

It is fair to say that Coinbase simultaneously faces significant competitive challenges and historical opportunities. This is Mint Ventures’ first report on Coinbase, and we will maintain long-term observation of the company.

Disclaimer: This report reflects the author’s thoughts as of the date of publication. Opinions may change over time and are highly subjective. Errors in facts, data, or reasoning may exist. Nothing in this report should be considered investment advice. Feedback and further discussion from peers and readers are welcome.

2. Company Overview

2.1 Development History and Milestones

Coinbase was founded in 2012 by Brian Armstrong and Fred Ehrsam, with its headquarters in San Francisco. In its early days, the company focused on Bitcoin brokerage services and, in 2014, obtained one of the first BitLicenses issued by the state of New York.

Since then, Coinbase has continuously expanded its product offerings: in 2015, it launched the trading platform “Coinbase Exchange” (later rebranded as Coinbase Pro); in 2016, it began supporting trading of multiple crypto assets, including Ethereum. In 2018, the company entered the blockchain application space through acquisitions such as Earn.com and brought on Emilie Choi, a former LinkedIn executive, to lead its M&A strategy. In 2019, Coinbase acquired Xapo’s institutional business, cementing its leading position in custody services. That same year, its valuation surpassed $8 billion. On April 14, 2021, Coinbase successfully went public on Nasdaq, becoming the first major crypto exchange to list (and remains the only one to date), with its market capitalization exceeding $85 billion at one point. After going public, the company continued to expand globally and diversify its product line: in 2022, it acquired futures exchange FairX and entered the crypto derivatives market, and also launched an NFT marketplace (although trading volume later remained subdued). In 2023, Coinbase launched Base, an Ethereum Layer 2 network, to strengthen its on-chain ecosystem. The company also actively pursued regulatory approvals, obtaining licenses in multiple jurisdictions, including Singapore, the EU (Ireland), and Brazil, and in 2025, it completed the acquisition of leading options trading platform Deribit.

After more than a decade of development, Coinbase has grown from a single Bitcoin brokerage into a comprehensive crypto financial platform offering trading, custody, payments, and more.

2.2 Positioning and Target Customers

Coinbase’s mission is to “increase economic freedom in the world,” with a vision to modernize the century-old financial system and enable anyone to participate in the crypto economy in a fair and accessible way. The company positions itself as a secure and trusted one-stop platform for crypto assets, attracting retail users through simple and intuitive products while providing institutional-grade services to meet the needs of professional investors.

Coinbase’s customer base can be broadly categorized into three groups:

- Retail Users: Individual investors interested in crypto assets. Beyond trading mainstream cryptocurrencies, Coinbase also offers features such as staking for yield generation, payments, and other utilities. Its Monthly Transacting Users (MTUs) peaked at 11.2 million in Q4 2021. Even during the market downturn in 2022–2023, it maintained a solid base of over 7 million quarterly active users. In Q1 2025, MTUs reached around 9.2 million, before slightly declining to approximately 9.0 million in Q2 2025.

- Institutional Clients: Since 2017, Coinbase has expanded aggressively into the institutional market by offering brokerage services via Coinbase Prime and custody solutions through Coinbase Custody. Clients include hedge funds, asset managers, and corporate treasury departments. By the end of 2021, Coinbase had over 9,000 institutional clients, including 10% of the world’s top 100 hedge funds. Institutions now account for the majority of trading volume on the platform (about 81% in 2024). Although fee rates are lower than for retail users, this segment contributes stable revenue streams through custody fees and trading income.

- Developers and Ecosystem Partners: Coinbase also treats developers and blockchain projects as ecosystem clients. Through “Coinbase Cloud,” the company provides infrastructure services such as node hosting and API access to support blockchain network development. In addition, Coinbase partners with new projects via listings and investments. Notably, the USDC stablecoin was co-launched by Coinbase and Circle. Coinbase plays dual roles as both an issuance partner and a major distribution platform, capturing significant revenue from interest income and channel fees shared with Circle.

Overall, Coinbase combines mass-market accessibility with institutional trust, bridging retail and institutional markets. Within the crypto ecosystem, it serves as a critical “gateway between the fiat and crypto worlds.”

2.3 Equity and Voting Rights Structure

The company adopts a dual-class share structure (Class A and Class B). Class A common shares are listed on Nasdaq, carrying one vote per share, while Class B common shares—held by the founders and executives—carry 20 votes per share. Founder and CEO Brian Armstrong holds approximately 23.48 million Class B shares, controlling over 64% of total voting power, which makes Coinbase a tightly controlled company. A small portion of Class B shares is also held by early investors such as Andreessen Horowitz. In mid-2025, Armstrong converted and sold a small number of his Class B shares but still retained roughly 469.6 million votes, equivalent to the voting power of Class A shares. Since Class B shares can be converted into Class A shares at a 20:1 ratio at any time, the company’s total share count may fluctuate slightly with conversions.This dual-class structure secures the founding team’s control over Coinbase’s strategic direction but also limits the influence of ordinary shareholders in corporate governance. Overall, Coinbase’s ownership is highly concentrated, with significant decision-making power in the hands of the founder, ensuring alignment in long-term vision and strategy.

3. Industry Analysis

3.1 Market Definition and Segmentation

Coinbase operates in the broader cryptocurrency trading and related financial services market. The core segments include:

- Spot Trading Market: The buying and selling of crypto assets via order matching, which remains Coinbase’s core business. By trading pair, the market can be segmented into fiat-to-crypto (on-ramp) and crypto-to-crypto transactions. By customer type, it can be divided into retail and institutional trading.

- Derivatives Trading Market: Includes leveraged products such as cryptocurrency futures and options. This market has expanded rapidly in recent years, with crypto derivatives accounting for about 75% of total trading volume in H1 2025 (source: Kaiko). Coinbase entered the derivatives business relatively late and currently operates through a regulated futures exchange as well as international platforms.

- Custody and Wallet Services: Provide secure storage solutions for institutions and individuals holding significant amounts of crypto assets. The custody business is closely tied to trading, as clients engaging in large transactions on exchanges often require compliant custody arrangements.

- BlockchainInfrastructure and Other Services: Covers stablecoin issuance and circulation, blockchain operations (e.g., Base), payments and settlements, and staking. These “crypto-financial” services expand revenue sources beyond trading. For instance, Coinbase generates interest and fee income from the USDC stablecoin and staking operations.

3.2 Historical Scale and Growth (Past Five Years)

The overall cryptocurrency market has exhibited pronounced cyclical volatility. Measured by trading volume, the global crypto trading market expanded from approximately USD 22.9 trillion in 2017 to USD 131.4 trillion in 2021, representing an exceptionally high compound growth rate. Subsequently, volumes contracted to USD 82 trillion in 2022 amid a market downturn (–37% YoY) and further slipped to USD 75.6 trillion in 2023. In 2024, fueled by a new wave of market enthusiasm, the total annual trading volume rebounded to a record high of about USD 150 trillion—nearly doubling from 2023.

Industry scale is highly correlated with crypto asset prices and volatility. For example, in the 2021 bull market, token prices surged and speculative trading flourished, driving a YoY trading volume increase of nearly +196%. Conversely, in the 2022 bear market, depressed prices triggered a sharp decline of almost 40% in trading activity.From a user perspective, the global crypto ownership base has also fluctuated with market cycles but shows a long-term upward trend. According to research by Crypto.com, the number of global crypto users rose from roughly 50 million in 2018 to over 300 million in 2021, contracted somewhat in 2022, and then recovered to around 400 million by the end of 2023.

Coinbase’s own performance has closely tracked industry dynamics. Platform trading volume grew from USD 32 billion in 2019 to USD 1.67 trillion in 2021, before falling to USD 830 billion in 2022 and further to USD 468 billion in 2023. On the user side, Coinbase’s Monthly Transacting Users (MTUs) increased from under 1 million in 2019 to an annual average of 9 million in 2021, then moderated to the 7–9 million range per quarter during 2022–2023.

In summary, over the past five years, the industry has demonstrated substantial medium- to long-term growth, albeit with sharp cyclical fluctuations.

3.3 Competitive Landscape & Coinbase Market Share (Past Five Years)

The cryptocurrency exchange industry is highly competitive, with market dynamics shifting alongside broader industry cycles.

Globally, Binance has rapidly risen since 2018 to become the largest exchange by trading volume. At its bull-market peak, Binance’s spot market share exceeded 50%; as of early 2025, it still maintained around 38%, ranking first. Other major players include OKX, Coinbase, Kraken, Bitfinex, and regional leaders such as Upbit in Korea. In recent years, emerging platforms such as Bybit and Bitget have also gained meaningful market share. Coinbase’s global market share has generally fluctuated in the 5–10% range. For instance, in H1 2025, Coinbase accounted for roughly 7% of the combined spot trading volume among the global top 10 exchanges, on par with OKX and Bybit. By comparison, Binance’s share was several times higher. It is important to note that Coinbase’s focus on the regulated U.S. market—and its decision not to engage in aggressive listing of speculative tokens—has limited its global ranking relative to more aggressive or wash-trading–prone competitors. However, in fiat-to-crypto on-ramp services and the U.S.-regulated market, Coinbase holds a clear advantage. Since 2019, Coinbase has consistently ranked as the largest exchange by trading volume in the U.S., and further strengthened its U.S. spot and derivatives market share in 2024. Following the collapse of FTX in 2022, Coinbase’s position in the U.S. has become even more dominant.

Market Dynamics over the Past Five Years

Several notable shifts have occurred:

- Market share concentration followed by fragmentation: After FTX’s collapse in 2022, Binance’s global market share surged from 48.7% in Q1 to 66.7% in Q4. Since then, its dominance has eroded, with Bybit, OKX, Bitget and others steadily gaining share, intensifying competition.

- Rising regulatory pressure driving regional divergence: In the U.S., heightened compliance requirements have reduced the number of viable exchanges (leaving primarily Coinbase and Kraken). In contrast, Asian platforms have grown rapidly, with Upbit becoming dominant in South Korea and Gate.io expanding across Southeast Asia.

3.4 Industry Scale and Growth Outlook (Next 5–7 Years)

Looking ahead over the next 5–7 years, the cryptocurrency trading industry is expected to continue expanding, though the pace of growth will depend on multiple factors and scenario assumptions. Industry research reports (from SkyQuest, ResearchAndMarkets, Fidelity, Grand View Research, etc.) generally project the crypto market to sustain a double-digit CAGR.Under the base-case scenario—assuming macroeconomic stability and no severe deterioration in regulatory conditions—the total global crypto market capitalization could rise from the current level of just over USD 3 trillion to the USD 10 trillion range by 2030. Trading volumes are likewise expected to increase significantly; however, as the market matures, volatility may decline, leading to trading volume growth slightly lagging behind market cap growth. We forecast an average annual growth rate of around 15% in trading activity.

Key growth drivers for the industry include:

- Asset Price Trends: Continued new highs in leading assets such as Bitcoin would lift the broader market. Rising prices and higher volatility tend to stimulate trading activity, amplifying transaction volumes.

- Derivatives Penetration: With derivatives already accounting for ~75% of total trading volumes, further expansion is expected. Institutional investors favor futures and other hedging tools, while retail adoption of leveraged products is also likely to increase. Assuming the derivatives share rises to 85% by 2030, overall trading volume could be boosted by an additional 1.2x or more.

- Institutional Adoption: Greater participation from traditional financial institutions (asset managers, banks, etc.) could introduce trillions of dollars in new capital. Examples include broader ETF approvals, institutional access channels (many are still restricted from holding direct crypto exposure, even via ETFs), and potential allocations from sovereign wealth funds. Such inflows would significantly deepen market liquidity and drive demand for both trading and custody. Fidelity, for instance, projects institutional capital inflows to add hundreds of billions of dollars annually to crypto market cap over the coming years.

- Regulatory Clarity: Clear and consistent regulatory frameworks will reduce participation risks and attract new entrants. In an optimistic scenario, major economies implement well-defined licensing regimes, expand ETF availability, and broadly legalize institutional participation—leading to higher user adoption and activity. In a pessimistic scenario, restrictive policies (e.g., banking access limits, strict capital requirements) could cap or stall growth. At present, regulatory clarity appears to be improving: the passage of the U.S. Genius Stablecoin Act and the Clarity Act in the House have created a positive precedent that may influence other developed economies. Overall, the global policy trajectory toward clearer rules is encouraging.

Scenario Analysis: Industry Outlook 2025–2030

- Base Case: Assuming a stable macro environment and cautious but supportive regulation in major economies, crypto assets gradually gain wider investor acceptance. Under this scenario, market capitalization grows at an annual rate of around 15%, while trading volumes expand at 12% CAGR. By 2030, total annual global trading volume could reach approximately USD 300 trillion, with industry revenues (primarily trading fees) rising accordingly. Leading regulated platforms such as Coinbase are expected to see steady gains in market share. The industry experiences healthy, sustainable growth without excessive bubbles.

- Optimistic Case: Assuming a boom similar to the “fintech” wave, major economies (especially the U.S.) establish clear regulatory frameworks, large institutions and corporates enter aggressively, and crypto technologies achieve broad adoption (e.g., rapid growth and mass adoption of DeFi). Asset prices surge (with Bitcoin potentially reaching the USD 1 million level by 2030, in line with long-term projections from ARK Invest). Market capitalization grows at 20%+ CAGR, and trading volumes at 25% CAGR. Under this projection, annual trading volume could soar to USD 600–800 trillion by 2030. Regulated giants such as Coinbase capture outsized profits in this explosive growth phase, with industry ceilings raised substantially.

- Pessimistic Case: Assuming adverse macro conditions or heavy regulatory headwinds—for example, strict restrictions from major countries—crypto assets remain in prolonged stagnation. Industry scale may plateau, grow only marginally, or even contract in some years. In the worst case, trading volume growth slows to low single digits, stagnates, or turns negative, leaving annual volumes stuck at USD 100–150 trillion by 2030. While Coinbase and other regulated exchanges may gain market share (as unregulated competitors are squeezed out), their absolute business growth would remain limited.

Overall Outlook:We lean toward a base-to-slightly-optimistic scenario: the crypto trading industry is likely to continue its cyclical yet upward trajectory over the next 5–7 years, with total scale rising year by year. Crypto users and industry coalitions have already become a political force that cannot be ignored in many countries—most notably in the 2024 U.S. elections, where Republican momentum against the Democrats was strongly supported by the crypto community. Since then, Democrats have taken a noticeably softer stance on crypto legislation requiring bipartisan support. In fact, many Democratic lawmakers voted in favor of both the Genius Act (passed by both chambers) and the Clarity Act (passed in the House), underscoring a structural shift toward regulatory moderation.

4. Business and Product Lines

Coinbase currently operates a diversified business model, with revenue primarily derived from two major segments: Trading and Subscriptions & Services, each supported by multiple product lines. Below we outline the business model, key metrics, revenue contribution, profitability, and future roadmap of its major businesses.

- Retail Trading (Brokerage Business):

- Future roadmap: Coinbase is expanding its retail offerings to increase user stickiness. Initiatives include the Coinbase One subscription service (providing zero-fee trading allowances and premium features), continued expansion of tradable tokens (48 new assets listed in 2024, including popular meme coins to drive traffic), and enhanced user experience (simplified interfaces, educational content). The company is also exploring social trading and automated investment tools. With market recovery, retail trading will remain the cornerstone of Coinbase’s revenue base, with growth depending on broader market sentiment and Coinbase’s ability to capture market share.

- Professional & Institutional Brokerage: This segment encompasses trading services for high-net-worth individuals and institutional clients, primarily through Coinbase Prime and the now-integrated Coinbase Pro platform. These professional platforms offer deep liquidity, lower fees, and API access to attract large-volume traders and market makers. Institutional trading accounts for the majority of Coinbase’s volume—80–90% of total (e.g., in 2024 institutional trading volume reached $941 billion, or 81% of the total). However, with fee rates typically ranging from a few basis points to 0.1%, the direct revenue contribution is modest—about 10% of total trading revenue in 2024. That said, the indirect benefits of institutional business are substantial: institutions often leave significant assets under custody at Coinbase and participate in staking programs, generating custody fees, interest income, and financing revenues. Moreover, active institutional participation enhances platform liquidity and improves price discovery, ultimately benefiting retail users’ trading experience. Key metrics include institutional client count and Assets Under Custody (AUC). Coinbase’s AUC peaked at $278 billion in Q4 2021, fell to $80.3 billion by end-2022 amid the market downturn, then rebounded to ~$145 billion by end-2023. Entering 2025, institutional custody momentum remained strong: Q1 2025 average AUC reached $212 billion, up $25 billion QoQ,Q2 2025 set another record at $245.7 billion. Profitability: While institutional trading itself has limited direct margin contribution, custody, financing, and staking services meaningfully expand revenue streams.

- Future roadmap: Coinbase is scaling its derivatives offering to meet institutional demand. In 2023, it launched perpetual futures for overseas clients and, via its U.S. broker subsidiary, secured approval to offer Bitcoin and Ethereum futures to U.S. institutions. Coinbase also established Coinbase Asset Management (via the 2023 acquisition and restructuring of One River Asset Management), with plans to launch crypto investment products such as ETFs and index baskets to broaden institutional participation. A landmark step came in late 2024 when Coinbase announced the $2.9 billion acquisition of Deribit, the world’s leading crypto options exchange (deal structure: ~$700 million in cash plus 11 million shares of Coinbase Class A common stock). This transaction marked one of the largest M&A deals in crypto industry history, aimed at rapidly strengthening Coinbase’s global derivatives presence. Deribit processed $1.2 trillion in options trading volume in 2024, up 95% YoY, and dominates the market with over 87% share in Bitcoin options. Through this integration, Coinbase gained immediate leadership in Bitcoin and Ethereum options markets. Together with its futures and perpetual contracts, the acquisition significantly broadens Coinbase’s institutional derivatives portfolio, reinforcing its position as the go-to platform for institutions entering the crypto space.

- Custody and Wallet Services:

- Future roadmap: Coinbase plans to continue investing in custody technology and security to meet regulatory requirements (e.g., the New York Trust license under regulated Custody Trust). The company also aims to expand custody services across additional asset classes and geographies, including institutional staking and custody for ETFs. In 2024, Coinbase was selected as the custodian for multiple Bitcoin spot ETFs.

- Subscriptions & Services Revenue (Staking, USDC Interest, etc.): In recent years, Coinbase has focused on developing a diversified revenue stream under the Subscriptions & Services segment. Key components include:

- Staking Services: Users delegate their crypto holdings via Coinbase to participate in blockchain staking and earn network rewards. Coinbase collects a commission (typically ~15%) from these rewards. Staking provides users with passive income while generating revenue for the platform. Since mainstream assets like Ethereum opened for staking in 2021, this revenue line has grown rapidly.

- Stablecoin Interest Income (USDC): Interest earned on USDC has become a significant revenue contributor for Coinbase in recent years. In 2023, with rising interest rates and expanded USDC reserves, Coinbase generated approximately $695 million in USDC interest income, representing about 22% of total revenue, significantly higher than in prior years. In 2024, as USDC market rates and circulation continued to increase, Coinbase’s annual USDC-related interest income rose to around $910 million, up 31% YoY. Although its share of total revenue declined to ~14%, the absolute amount reached a new high. By Q2 2025, Coinbase reported $333 million in stablecoin interest income, accounting for 22.2% of quarterly revenue. This stable income primarily comes from Coinbase’s revenue-sharing agreement with Circle: interest generated from USDC reserves is split 50/50, and interest from USDC held on Coinbase’s platform accrues 100% to Coinbase. As a result, USDC interest has become the fastest-growing and largest single line within Coinbase’s Subscriptions & Services segment, providing a recurring revenue source beyond transaction fees.

- In 2023, Coinbase strengthened its strategic collaboration with Circle, making significant adjustments to the joint operation model under Centre, the governance entity originally created by both parties. As part of this restructuring, Coinbase acquired equity in Circle, becoming one of its minority shareholders. Specifically, Circle purchased the remaining 50% stake in Centre Consortium held by Coinbase for approximately $210 million in Circle stock, in exchange granting Coinbase equivalent economic interest and certain governance influence. Following the transaction, the Centre Consortium was dissolved, and Circle assumed sole responsibility for USDC issuance and governance. Despite Circle taking over full management, Coinbase’s influence in the USDC ecosystem increased, as the new agreement grants Coinbase substantive participation and veto rights on major USDC strategies and partnerships, including a single-vote veto on any proposed USDC partnership agreements, ensuring that Coinbase’s interests remain aligned with USDC’s development. Furthermore, adjustments to the revenue-sharing mechanism, particularly the division of interest income, have strengthened the incentives for both parties to promote USDC adoption. These measures have encouraged Coinbase to actively support USDC by listing it on additional blockchains and offering incentives and rewards across its international exchanges and wallet products, such as higher yields for USDC holdings. Overall, the 2023 equity investment and agreement restructuring significantly strengthened Coinbase’s alliance with Circle, enabling Coinbase to participate more deeply in USDC governance while simultaneously promoting its adoption, jointly expanding the market influence and capitalization of this regulated stablecoin.

- Other subscription services include Coinbase Earn, which rewards users for engaging with educational content, Coinbase Card, which offers cashback on debit card transactions, and Coinbase Cloud, which provides blockchain infrastructure services. Although currently small in scale, these services offer business synergies and align with Coinbase’s strategy of building a comprehensive crypto platform. For example, Coinbase Cloud supplies nodes and exchange APIs to institutions and developers, supporting the launch of multiple blockchain networks in 2024, and has the potential to evolve into an “AWS-like” business within the crypto sector over the long term.

- The Subscriptions & Services segment has grown significantly, rising from less than 5% of total revenue in 2019 to approximately 40–50% today, serving as a stable revenue source during periods of weak trading activity. Gross margins are very high, approaching 90%, due to the low costs associated with interest and fee-based income. Looking ahead, Coinbase plans to continue expanding this segment by introducing more subscription packages for high-frequency users, supporting a broader range of stakable assets, and deepening the global adoption of USDC, including innovations such as using USDC as margin for U.S. futures trading. This segment is expected to become an important stabilizer against trading volatility.

- Decentralized Business: Base Layer-2 Network

- Positioning and Vision: Base is an Ethereum Layer-2 network launched by Coinbase in August 2023, built on the Optimism OP Stack, with the goal of smoothly onboarding over 100 million Coinbase users into the on-chain ecosystem. According to the official roadmap as of January 2025, Base plans to achieve sequencer decentralization by the end of 2025 and share network revenue through community governance.

- Key Operational Metrics: As of August 2025, Base’s on-chain assets totaled approximately $15.46 billion, with 30.7 million monthly active addresses, 9.24 million daily transactions, and $204,000 in daily on-chain fee revenue, ranking first among all Layer-2 networks.

- Revenue Contribution: Coinbase classifies Base sequencer fees as “other trading revenue.” In 2024, Base contributed roughly $84.8 million to Coinbase (Tokenterminal data; not specifically disclosed in official financial statements), with revenue reaching $49.7 million year-to-date in 2025. Base has become one of Coinbase’s most promising on-chain revenue engines beyond trading fees and interest income.

- Other Potential Business Lines: Coinbase is also exploring new opportunities, such as the NFT marketplace launched in 2022 (Coinbase NFT), which saw low user engagement and had investment scaled back in 2023, and payment and merchant tools like Coinbase Commerce, which allows merchants to accept crypto payments and primarily serves as a strategic initiative. While these businesses currently contribute minimally to financials, they are strategically important for completing the ecosystem and enhancing user reliance on the Coinbase platform.

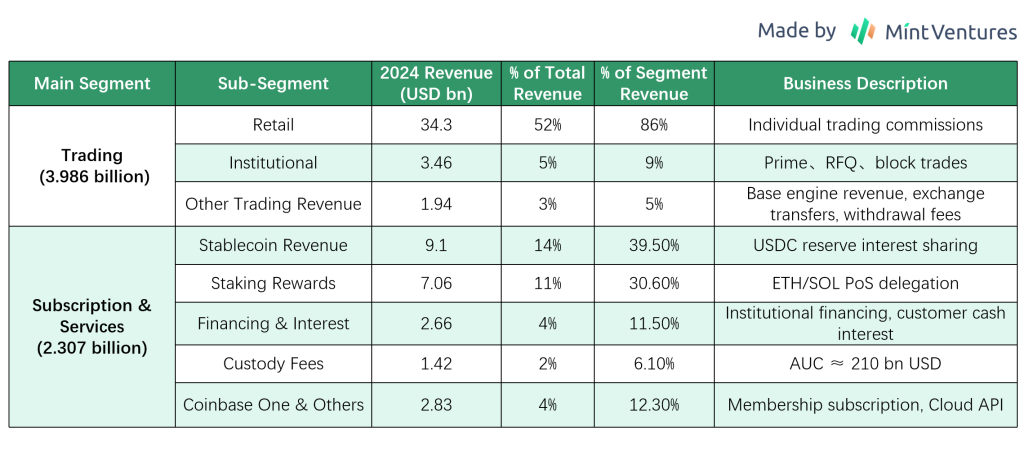

The table below shows Coinbase’s 2024 revenue composition and segmental contributions.

Summary of Business and Product Lines

Coinbase’s business has expanded from a single trading platform to a multi-engine model encompassing trading, custody, staking, and stablecoins. This diversification has reduced reliance on trading fees—with non-trading revenue accounting for 40% of total revenue in 2024—while also enhancing customer stickiness, as users keep assets on the platform to earn staking rewards or utilize stablecoins, reducing the likelihood of migration elsewhere. The various business lines create synergies: trading drives asset retention, retained assets generate staking and interest income, which in turn incentivizes further trading. This “flywheel effect” is a key component of the moat Coinbase is building. However, the company must carefully balance regulatory compliance and resource allocation to ensure sustainable operations; for instance, staking and lending must comply with securities laws, and stablecoins require transparent reserves. Overall, Coinbase’s product line is comprehensive, positioning it as one of the first firms in the industry to build an integrated crypto financial services platform, providing a relatively stable revenue structure and growth path in a highly competitive market.

5. Management and Governance

In evaluating Coinbase’s management, we focus on several dimensions: the background and stability of the executive team, and the quality of past strategic decisions.

5.1 Core Management Team Background

- Brian Armstrong – Co-founder, Chief Executive Officer (CEO), and Chairman of the Board, holding the majority of voting power in the company. Born in 1983, Armstrong previously worked as a software engineer at Airbnb. He founded Coinbase in 2012 and is one of the earliest entrepreneurs in the crypto space. Armstrong emphasizes the company’s long-term mission and product simplicity, and is known internally for adhering to principles, such as the “no politics” cultural statement issued in 2020.

- Fred Ehrsam – Co-founder and Board Member. Formerly a foreign exchange trader at Goldman Sachs, Ehrsam co-founded Coinbase with Armstrong in 2012 and served as its first president. He stepped down from day-to-day management in 2017 to establish the prominent crypto investment fund Paradigm, but remains on the board, providing guidance on industry trends and company strategy.

- Alesia Haas – Chief Financial Officer (CFO). Haas joined Coinbase in 2018, previously serving as CFO at hedge fund Och-Ziff (now Sculptor Capital) and as an executive at OneWest Bank, bringing extensive experience in traditional finance and capital markets. She led the company through IPO preparation, emphasized financial discipline, and implemented two rounds of layoffs in 2022 to control costs. Haas also oversees Coinbase subsidiary Coinbase Credit, exploring crypto lending initiatives.

- Emilie Choi – President and Chief Operating Officer (COO). Choi joined Coinbase in 2018 as VP of Business Development and was promoted to President and COO in 2020. Prior to Coinbase, she led M&A and investment at LinkedIn, including the acquisition of SlideShare, and is known for strategic expansion expertise. At Coinbase, Choi has driven multiple acquisitions (Earn.com, Xapo Custody, Bison Trails) and international expansion, making her one of the most influential executives after Armstrong. She also oversees daily operations, talent management, and strategic project execution.

- Paul Grewal – Chief Legal Officer (CLO). Joining in 2020, Grewal was previously Deputy General Counsel at Facebook and a former federal judge. He is responsible for managing Coinbase’s legal and regulatory matters, including litigation with the SEC in 2023. His team plays a key role in compliance and policy advocacy.

- Other Key Executives: The Chief Product Officer role was held by Surojit Chatterjee (former Google executive) from 2020 to 2022; after his departure in early 2023, product leadership has been managed by multiple department heads. The Chief Technology Officer (CTO) position has been held by Greg Tusar and others, with engineering executives collectively managing technology. Chief People Officer (CPO, HR) LJ Brock leads recruitment and cultural initiatives, while Chief Marketing Officer Kate Rouch (former Facebook marketing director) contributes cross-industry expertise.

Overall, the leadership team combines young, entrepreneurial founders with seasoned professionals from traditional finance and tech giants, enabling Coinbase to balance technological innovation with regulatory execution. All executives hold significant equity or stock options, and Armstrong benefits from a special CEO performance equity plan designed to incentivize achieving long-term market capitalization targets over ten years.

5.2 Personnel and Strategic Stability

Coinbase has experienced fluctuations in both personnel and strategy, but overall maintains consistency.

- Executive Turnover: Most of the core founding team remains in place (Armstrong and Ehrsam on the board). However, in recent years, some executives have departed: for example, former Chief Product Officer Surojit Chatterjee left in early 2023, and the CTO and Chief Compliance Officer roles have seen several changes. Some turnover was market-driven—during the 2022 bear market and performance downturn, management was streamlined. Additionally, after Armstrong announced the “no politics” policy in 2020, about 60 employees were laid off, including the former Chief People Officer. Despite this, the top leadership has remained largely stable: the CEO, CFO, and COO have served for many years and led the company through its IPO, while the legal head has maintained continuity. This indicates a relatively mature management team with key positions experiencing minimal disruption.

- Strategic Direction Consistency: Since its founding, Coinbase’s core mission—to build a trusted crypto financial ecosystem—has remained unchanged. Strategic priorities have evolved with the industry but maintain a clear trajectory: early focus on Bitcoin brokerage and user growth, followed by expansion of supported assets and international markets. Since 2020, Coinbase has pursued a dual-track strategy: serving both retail and institutional clients while growing subscription-based revenue to diversify its business model. Even during market downturns (e.g., 2018 and 2022), the management continued investing in new products, such as launching USDC in 2018 and entering the NFT platform and derivatives space in 2022, demonstrating confidence in the long-term crypto trend. Corrections have been made where needed—for instance, scaling back the NFT initiative in 2023 after weak adoption, and implementing two rounds of layoffs totaling ~2,100 employees (~35% of staff) in FY2022 after over-hiring, which improved operational efficiency. Overall, Coinbase demonstrates strong strategic execution, without major missteps or disruptive pivots, aligning decisions with industry development.

- Strategic Alignment: Quantifying strategic consistency, such as tracking early positioning in key technologies and markets, shows that Coinbase has generally anticipated major industry trends: supporting Ethereum as early as 2015 (betting on smart contracts), launching the stablecoin USDC in 2018 (positioning for compliant stablecoins), applying for futures licenses in 2021 (forward-looking on derivatives), and later developing its own L2 network. These moves have largely aligned with industry evolution, reflecting strong management judgment. There have been missteps, such as missing the early DeFi and decentralized exchange (DEX) wave in 2019–2020, only later entering through Base; however, given Coinbase’s focus on compliance, this may have been a deliberate strategic choice.

5.3 Strategic Capability Review

Key examples of successes and missteps in Coinbase management’s decision-making include:

- Strategic Successes: Coinbase has long prioritized compliance. Since its founding, the company proactively applied for FinCEN registration and state licenses in 2013. This early emphasis on regulatory adherence proved prescient: while competitors were forced to exit the U.S. market due to compliance issues, Coinbase had already established a regulatory moat and earned strong trust from domestic users (the company has never experienced major client fund theft), expanding its U.S. market share. Another success was the timing of the IPO—management capitalized on the 2021 bull market peak to go public, providing ample capital and brand credibility, while rewarding early investors and employees, thereby stabilizing morale. The acquisition strategy has also been effective, such as the 2019 purchase of Xapo’s institutional custody business, which quickly positioned Coinbase as one of the largest crypto custodians globally, securing a first-mover advantage in the institutional market. These examples demonstrate the management team’s strategic vision and execution capability.

- Strategic Missteps: Rapid expansion led to layoffs. During the 2021 bull market, Coinbase’s headcount surged from roughly 1,700 to nearly 6,000 by early 2022 (currently around 3,700), resulting in overstaffed departments. Armstrong publicly acknowledged that the aggressive hiring led to efficiency decline. When the market cooled in 2022, the company had to implement two rounds of large-scale layoffs, impacting morale. Another setback was the NFT Marketplace launch—Coinbase invested in the NFT platform in April 2022, aiming to replicate OpenSea’s success. However, late entry, lack of differentiation, and a cooling NFT market led to persistently low monthly transaction volume, and the company eventually largely abandoned operations. While management’s experimental initiatives did not always meet expectations and some market judgments were off, overall losses were limited and corrective actions were timely.

Overall, Coinbase demonstrates solid management capability. Core team members remain stable, strategic judgment generally aligns with industry trends, and the company has not missed major opportunities. While there have been occasional cost-control issues and product exploration failures, these do not overshadow the team’s overall effectiveness.

6. Operations and Financial Performance

This section focuses on Coinbase’s revenue, profitability, costs, and balance sheet to assess the company’s earnings quality and financial stability.

6.1 Income Statement Overview (5 Years)

Coinbase’s revenue and profit performance is highly dependent on crypto market conditions, exhibiting “rollercoaster” volatility.

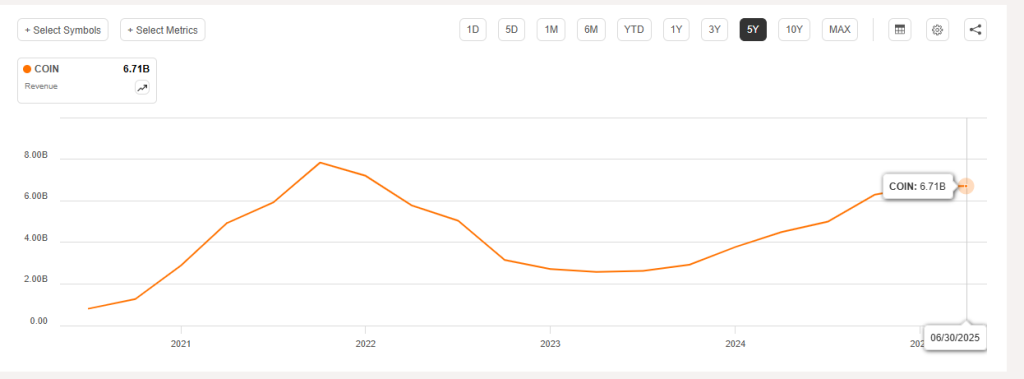

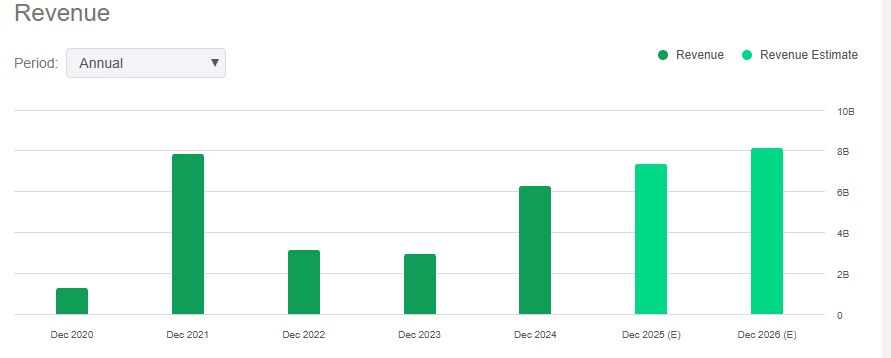

- Revenue: In 2019, total revenue was only $534 million. It rose to $1.28 billion in 2020, driven by a Bitcoin mini-bull market (+140%). The 2021 bull market saw revenue surge to $7.84 billion (+513% YoY). During the 2022 bear market, revenue sharply dropped to $3.15 billion (-60%) and further declined to $2.92 billion in 2023. With market recovery in 2024, revenue rebounded strongly to $6.564 billion, roughly doubling compared with 2023. In Q1 2025, Coinbase continued the strong momentum from late 2024, achieving total revenue of about $2.03 billion, a 24% YoY increase. In Q2 2025, revenue declined sequentially to approximately $1.5 billion, down 26% from Q1 2025, primarily due to a 16% drop in crypto market volatility, which weakened investor trading activity. This demonstrates that Coinbase’s revenue remains highly sensitive to market fluctuations, with noticeable short-term swings. However, compared to the same period last year, total revenue for the first half of 2025 still grew by around 14%. Overall, over the past five years, the company’s revenue has shown “rollercoaster” behavior with extreme cyclicality: from 2019 to 2024, the compound annual growth rate (CAGR) was about 40%, but annual fluctuations exceeded ±50%, reflecting bull-market spikes and bear-market halving, trends that continue to be evident in the first half of 2025.

- Revenue Composition: Trading fees have long been Coinbase’s primary revenue source, but their share has gradually declined. In 2021, trading revenue was $6.9 billion, accounting for about 87% of total revenue; in 2022, it fell to $2.4 billion (77%); in 2023, trading revenue dropped further to $1.5 billion (52%); and in 2024, it rebounded to approximately $4.0 billion (about 61%). Correspondingly, subscription and services revenue—which includes staking, interest, custody, etc.—rose from less than 5% in 2019 to 48% in 2023, before slightly declining to about 35% in 2024 (absolute value $2.3 billion).In Q1 2025, trading fee revenue was approximately $1.26 billion (+17.3% YoY), accounting for over 60% of quarterly revenue, while subscription and services revenue reached $698 million (+37% YoY), contributing more than 30% of revenue, mainly driven by rising USDC stablecoin interest income and growth in Coinbase One subscribers. In Q2 2025, trading and subscription revenue shifted in opposite directions: trading fees totaled about $764.3 million (around 54% of total revenue), while subscription and services revenue increased to $655.8 million (+9.5% YoY), rising to roughly 46% of total revenue—nearly matching trading revenue. Growth in the subscription segment was primarily fueled by USDC interest and custody services; Q2 average USDC reserves increased 13% from the previous quarter to $13.8 billion, generating substantial and stable interest income. Meanwhile, staking services and institutional custody fees continued steady growth, helping Coinbase’s subscription revenue reach record levels. For the first half of 2025, subscription and services revenue accounted for about 44% of total revenue, up significantly from 35% for the full year of 2024, further consolidating Coinbase’s business diversification. This shift in revenue composition reduces reliance on trading fees, helping mitigate the impact of sharp market fluctuations on overall revenue.

- Profitability: Benefiting from its high-margin business model, Coinbase’s profitability is extremely sensitive to trading volume. In 2019, the company still recorded a small loss of $30 million. In 2020, net profit reached $322 million (net margin 25%), and in 2021, net profit soared to $3.624 billion (net margin ~46%), exceeding the total profits of all prior years combined. However, in 2022, Coinbase suffered a massive net loss of $2.625 billion (net margin -83%), marking its worst year ever. In 2023, the company returned to modest profitability with a net income of $95 million (net margin 3%), and in 2024, net profit climbed to $2.579 billion (net margin ~39%), second only to the 2021 peak. This demonstrates that Coinbase’s profits fluctuate sharply in line with revenue. In Q1 2025, net profit was $66 million, appearing significantly lower than the previous quarter. However, this was mainly due to declines in the fair value of crypto assets, stock-based compensation, and litigation expenses. Adjusting for after-tax fair value changes in crypto investments and other one-time items, core operating net profit for the quarter was $527 million, more accurately reflecting operating performance. In contrast, Q2 2025 showed a dramatic spike: GAAP net profit reached $1.429 billion, a year-over-year surge (Q2 2024 net profit was only $36 million), with a net margin of about 95%. Yet, this unusually high profit primarily stemmed from non-recurring gains: $1.5 billion from the strategic revaluation of Coinbase’s equity stake in Circle and $362 million from crypto investment portfolio gains. After excluding these one-time items—and accounting for nearly $438 million of related tax adjustments—the adjusted Q2 net profit was only around $33 million, significantly lower than Q1’s $527 million, reflecting weakened core business profitability due to declining trading volume. Overall, Coinbase’s profitability remains highly cyclical: during bull markets, net margin can exceed 30–40% of revenue, whereas in downturns, losses can occur if cost control is insufficient. Nevertheless, the company’s ability to quickly return to break-even in 2023 following the massive 2022 loss—through layoffs and expense reductions—demonstrates operational flexibility and resilience.

- Expense Structure: On the cost side, Coinbase’s expenses are primarily composed of operating costs, including R&D, sales, and general administrative expenses, while direct trading costs are relatively small. Sales and marketing expenses typically account for less than 10% of revenue, and after 2022, they were further reduced to below 5%, reflecting disciplined marketing spending. Combined R&D and general administrative expenses make up roughly 20–30% of revenue, including substantial stock-based compensation (SBC) for employees. For example, during the 2021 IPO, a one-time equity-related expense was recognized, and from 2022 to 2023, annual SBC expenses remained around $300–500 million. The expense ratio (operating expenses as a percentage of revenue) is highly cyclical: it was significantly diluted during the bull market (around 22% in 2021) but spiked in the bear market (over 100% in 2022). Following layoffs and cost control, the ratio fell back to 70% in 2023. Since 2024, Coinbase has continued strict expense management, aligning staffing and project investment with business needs. Notably, in Q2 2025, a major data breach led to litigation and compensation expenses of approximately $307 million, causing total operating expenses to surge 15% quarter-over-quarter to $1.52 billion. Excluding this one-time event, core operating costs actually continued their downward trend. Stock-based compensation remains a significant portion of expenses and warrants ongoing attention: Q2 2025 SBC costs reached $196 million, up 3% from Q1, suggesting that annual SBC expenses could exceed $700 million. Overall, Coinbase’s expense structure is relatively flexible, with personnel and project spending adjustable according to market conditions, though the dilutive effect of stock-based compensation needs to be monitored.

6.2 Profitability and Efficiency (5-Year Overview)

Combining multiple ratio metrics to evaluate Coinbase’s profitability quality and operational efficiency:

- Gross Margin: Coinbase has maintained a high gross margin of 80–90% over the long term, reflecting the high-profit nature of its transaction fee business. For example, gross margin was approximately 88% in 2021, 81% in 2022, and rose to 84% in 2023 despite lower revenue (due to a higher proportion of interest income, which has minimal associated costs), reaching 85% in 2024. Even in Q2 2025, with declining trading volumes, gross margin remained around 83%. This indicates that regardless of market conditions, most of every dollar of revenue converts into gross profit, placing Coinbase ahead of peers (traditional securities brokers typically have gross margins of 50–60%).

- Net Margin: Net margin has been highly volatile. In 2021, net margin reached 46%, comparable to the most profitable tech companies; it fell to -83% in 2022 due to severe losses, recovered to 3% in 2023, and rose to 39% in 2024. In Q2 2025, adjusted net margin (excluding non-recurring items) was only about 2%. On average, during normal or bull market conditions, Coinbase’s net margin is around 30–40%, demonstrating strong profit leverage, but it can incur losses in downturns without timely cost reductions.

- ROE / ROA: Due to profit volatility, Return on Equity (ROE) and Return on Assets (ROA) fluctuate significantly. ROE exceeded 60% in 2021 (high profits combined with limited net asset expansion from the IPO), dropped to -40% in 2022, was below 2% in 2023, and rebounded to around 25% in 2024. ROA was about 20% in 2021 and approximately 15% in 2024, reflecting slightly lower efficiency after balance sheet expansion. Overall, Coinbase’s ROE during profitable years is far above that of traditional financial firms, though stability is weaker.

- Per-Employee Efficiency: Given the large fluctuations in headcount, revenue per employee is used to gauge efficiency. In the 2021 bull market, per-employee annual revenue reached approximately $1.9 million; it dropped below $500,000 in 2022, and after layoffs rebounded to $0.8–1 million per employee in 2023. This remains higher than most traditional financial institutions, indicating the scale economy of Coinbase’s digital platform model. With a reasonable workforce (currently around 3,700 employees), per-employee revenue is expected to stabilize around $1 million, potentially exceeding this in another super bull market.

6.3 Cash Flow and Capital Expenditures (5-Year Overview)

Coinbase’s operating cash flow is also cyclical, but overall remains positive.

- Operating Cash Flow (OCF): In 2021, OCF was very strong, with net cash inflow from operations of approximately $10 billion, mainly due to a surge in customer trading volume and resulting fund deposits. Free cash flow was substantially positive that year. In 2022, operating cash flow turned negative, with an outflow of about $2 billion, reflecting losses and changes in working capital. In 2023, through cost reductions and interest income, operating cash flow returned to positive, reaching approximately $520 million. In 2024, OCF surged, with net cash inflow from operations totaling $2.5 billion for the year, more than doubling year-over-year, driven by restored profitability and increased customer funds.

- Investing Cash Flow: As a light-asset company, Coinbase’s capital expenditures (CapEx) are relatively low, mainly allocated to acquisitions and platform R&D. From 2019 to 2021, annual CapEx averaged only tens of millions of dollars (for servers, office facilities, etc.). In 2022, CapEx increased to about $150 million (including office building purchases and data center expansion), and contracted again to roughly $50 million in 2023. Regarding acquisitions, the company spent significant cash around 2021 (e.g., acquiring Bison Trails and Skew for a total of about $100 million). Acquisitions slowed in 2022–2023. In 2024, Coinbase made smaller acquisitions, such as One River Asset Management. Overall, investing cash flow was a net outflow but not large enough to impact the company’s main operations. Additionally, from late 2024 to early 2025, Coinbase announced a major acquisition of the derivatives exchange Deribit, with a total deal value of approximately $2.9 billion, including $700 million in cash and the issuance of roughly 11 million shares of Coinbase stock.

- Free Cash Flow: Considering operating cash minus capital expenditures, Coinbase generates substantial free cash flow in profitable years: $9.7 billion in 2021, negative in 2022, recovered to about $400 million in 2023, and approximately $2.56 billion in 2024, demonstrating strong cash-generating capacity. Excess cash is primarily allocated to safe assets (e.g., short-term U.S. Treasury securities) or held in certain crypto assets.

- Financing Cash Flow: In 2021, Coinbase raised about $3.25 billion through convertible and corporate bonds, while its direct listing did not raise new equity. There were no major financing activities in 2022. In 2023, Coinbase proactively repurchased or retired part of its debt, buying back approximately $413 million at a discount to reduce interest expenses. The company has no dividend plans and only conducted small-scale stock repurchases at the end of 2022 and in 2023 to hedge equity incentives. Overall, the company’s financial policy is conservative and prudent.

- Cash Reserves: As of Q1 2025, Coinbase held approximately $9.9 billion in cash and cash equivalents. By Q2 2025, cash and equivalents had decreased to $7.539 billion, representing a notable drop but still maintaining a relatively healthy liquidity position.

6.4 Balance Sheet Stability (5 Years)

Coinbase’s balance sheet is relatively robust, characterized by high liquidity and low leverage.

- Debt Levels: During the 2021 bull market, the company issued debt twice: a $1.25 billion convertible bond maturing in 2026, and senior notes totaling $2.0 billion maturing in 2028 and 2031. This brought long-term debt to a peak of approximately $3.25 billion. Coinbase did not raise additional debt in 2022–2023, and by the end of 2023, debt had decreased to about $2.8 billion through repayments and buybacks. With adjusted EBITDA of approximately $3.35 billion in 2024, net debt/EBITDA was effectively zero (net cash position), and gross debt/EBITDA was less than 0.9x, reflecting very low leverage. Overall, the company’s liabilities have remained low post-IPO. Notably, as of 2024, Coinbase had not used any bank loans; all debt is in the form of publicly issued bonds with long maturities, minimizing short-term repayment pressure and eliminating refinancing risk.

- Liquidity: Coinbase holds substantial cash and cash equivalents, resulting in a very high quick ratio. Excluding customer deposits (which are backed by corresponding customer assets), the company’s core operating current assets significantly exceed its current liabilities. In the H1 2025 report, the quick ratio (excluding customer-related balances) exceeded 3.19x, meaning cash alone could cover over three times all short-term liabilities. Particularly, its USDC reserves are highly liquid and redeemable 1:1 for USD daily. In 2023, during a brief USDC de-pegging incident, Coinbase quickly honored customer redemptions without any liquidity squeeze.

- Asset Quality: Assets primarily consist of cash, cash equivalents, and short-term investments (high-grade bonds, etc.), accounting for over 60% of total assets. Proprietary crypto holdings are relatively modest; as of Q2 2025, the fair value of crypto assets held was $1.839 billion, composed of 11,776 BTC worth $1.261 billion (68.6%), 136,782 ETH worth $340 million (18.5%), and other crypto assets worth $238 million (12.9%). Relative to the company’s net asset base, this exposure is manageable, and price fluctuations are unlikely to significantly impair solvency.

Overall, Coinbase’s financial safety is high: low leverage, ample liquidity, and a balance sheet that has withstood multiple stress tests. Moreover, this strong balance sheet enables counter-cyclical investments during market downturns—for instance, during the 2022–2023 industry slump, the company maintained R&D and international expansion, supporting its long-term competitive position.

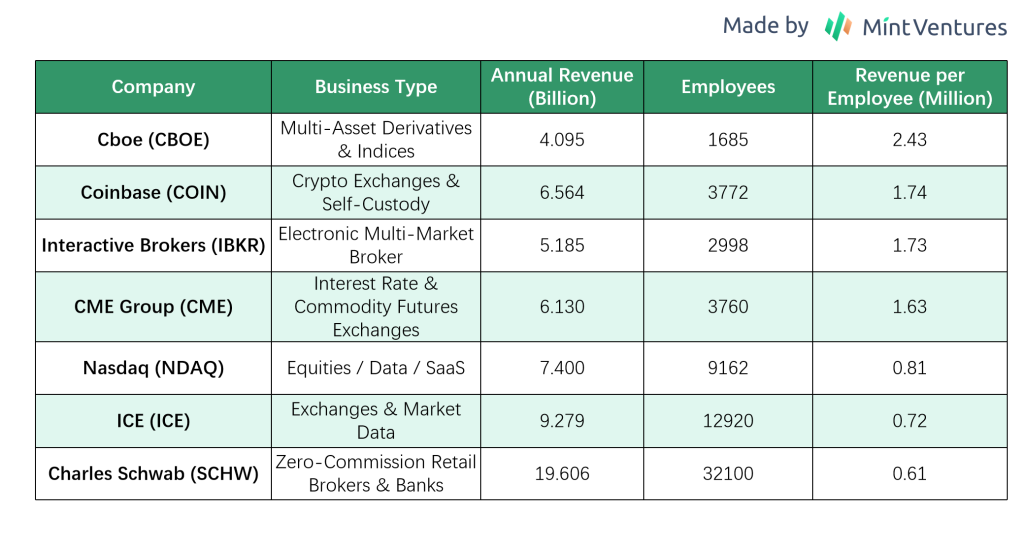

6.5 Peer Comparison

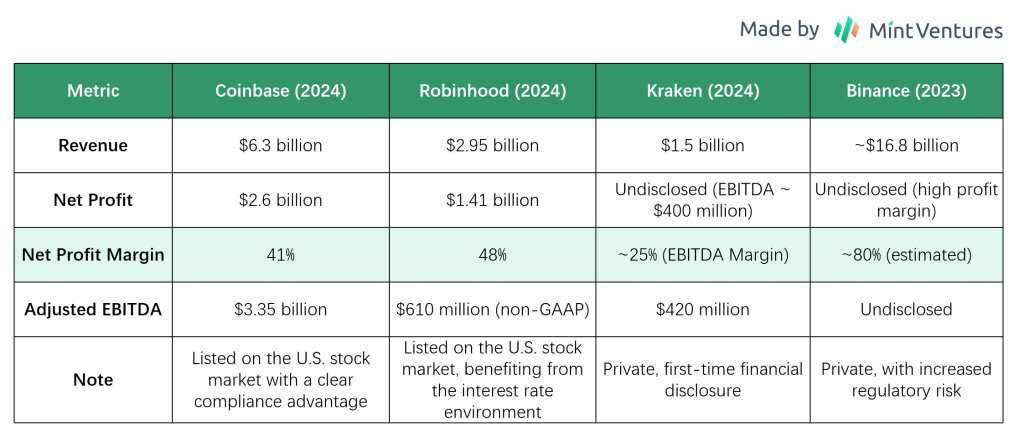

We compare Coinbase with other publicly listed or comparable trading platforms for 2024 and Q2 2025 financial metrics. The selected peers include Robinhood, Kraken, and Binance:

- Robinhood (U.S. stock brokerage & crypto trading platform): In 2024, Robinhood achieved net revenue of approximately $2.951 billion, up 58% year-over-year, recording its first full-year profit in history with net income of $1.411 billion (compared to a $541 million loss in 2023). The strong performance was driven by interest income boosted by high interest rates and a rebound in trading activity. Robinhood’s gross margin reached 94% in 2024, with a net margin of about 48%. In Q1 2025, revenue was $927 million (up 50% YoY), with net income of $336 million. With improving results, Robinhood’s stock price surged significantly from the end of 2024 to the present, giving it a market capitalization exceeding $95 billion.

- Kraken (U.S.-based established crypto exchange, privately held): In 2024, Kraken benefited from surging trading volumes, generating revenue of approximately $1.5 billion, up 128% YoY, close to a historical high. Adjusted EBITDA for the year was about $400 million, with an EBITDA margin of 25%-30%. As of the end of 2024, Kraken’s platform held assets worth $42.8 billion, with 2.5 million monthly active paying users, and average annual revenue per user exceeding $700. In Q1 2025, Kraken achieved revenue of $472 million (+19% YoY, slightly down 7% QoQ), while Q2 revenue was about $411.6 million, down 13% QoQ. As a private company, Kraken’s latest valuation is undisclosed; however, media reports indicate it sought over $10 billion in financing in 2021. Based on a $42.8 per share private equity price on the Hiive platform, its implied valuation is roughly $9.1 billion. Revenue growth in 2024 indicates significant expansion of its business scale, though its valuation multiples relative to revenue may be lower than those of publicly listed Coinbase and Robinhood.

- Binance (largest global crypto exchange, privately held): Binance, as the industry leader, far exceeds peers in trading volume and user base. Its financials are not regularly disclosed, but industry estimates suggest 2023 revenue reached approximately $16.8 billion, up 40% YoY, about 2.7 times Coinbase’s revenue for the same period. Binance reportedly generated over $12 billion in revenue and nearly $10 billion in profit in 2022, reflecting extraordinary profitability and scale (profit margin ~80%). As a private company, Binance does not have a publicly disclosed market cap or valuation multiple; however, based on its revenue and earnings, its implied market value could be in the hundreds of billions of dollars even under conservative multiples. Regulatory pressures in the U.S., Europe, and other regions add uncertainty to its future growth and potential pre-IPO valuation. Overall, Binance leads the industry in absolute scale, while regulated and listed platforms like Coinbase enjoy higher market confidence as reflected in valuation metrics such as price-to-sales and EV/EBITDA multiples, reflecting differences in regulatory transparency and business model.

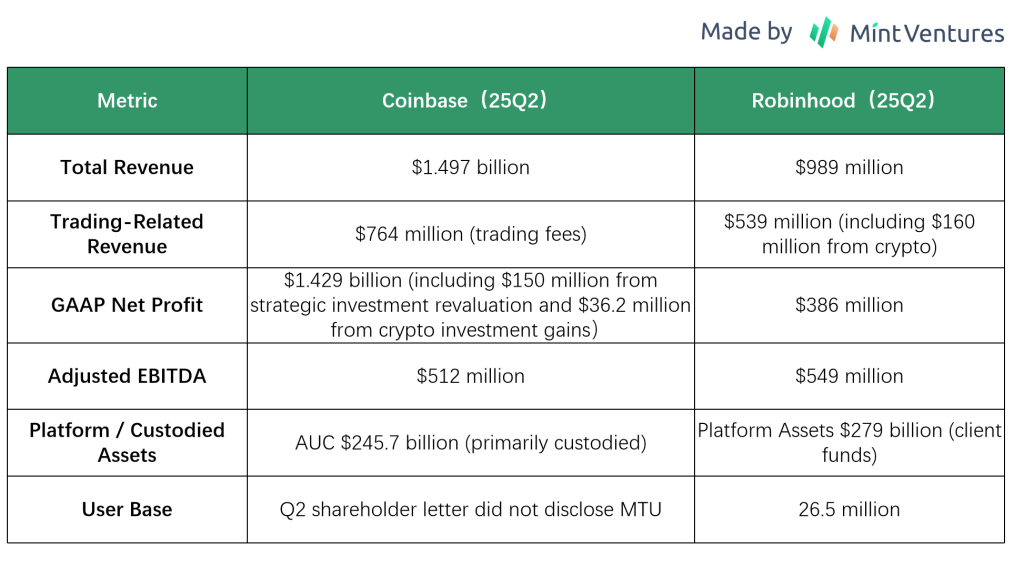

We now compare Coinbase and Robinhood’s Q2 2025 data:

Overall, the two companies have comparable revenue scales and other financial metrics. Coinbase’s current market capitalization is $79.8 billion, while Robinhood’s is $101.8 billion. However, their revenue structures differ significantly. Coinbase’s revenue comes from trading, subscriptions/custody/stablecoins/derivatives, whereas Robinhood’s revenue is derived from brokerage fees, interest income (spread from user funds deposited in banks and margin lending), and subscriptions/options/crypto trading. In recent years, Robinhood’s platform assets and user base have grown rapidly, and its acquisition of Bitstamp has accelerated international expansion, positioning it as a direct competitor to Coinbase both in the U.S. and globally.

In summary, Coinbase’s financial performance reflects the high-growth, high-volatility characteristics of the crypto industry. Yet, thanks to effective cost control and a strong balance sheet, the company has maintained resilience during market downturns and achieved outstanding profitability at market peaks. This performance elasticity is both an investment highlight and a risk factor: if the crypto market continues to perform well, Coinbase could potentially reach profit peaks similar to those in 2021. Conversely, in a market downturn, stricter expense management would be necessary to avoid repeating the losses of 2022. Currently, even if a new bull market emerges, the company maintains a lean workforce and controlled expenses. Going forward, close attention should be paid to whether the expansion of the subscription business can smooth out cyclical effects, making Coinbase’s financial performance more stable.

7. Competitive Advantages and Moat

Coinbase’s ability to maintain a leading position in the fiercely competitive crypto industry is closely tied to the multiple moats it has built:

Brand Trust and Regulatory Compliance Advantage

As one of the earliest exchanges to enter the regulated space, Coinbase has accumulated strong brand credibility. It is among the few exchanges in the U.S. to hold licenses in multiple states (since 2013, it has gradually obtained money transmission licenses in 46 states/territories, allowing legal operations across all 50 states), FinCEN registration, and the New York Trust License. Since its inception, Coinbase has never experienced a major loss of user assets. This has established a reputation for safety and reliability among users, an advantage that has become even more pronounced following incidents such as Mt. Gox, FTX, and other exchange collapses and hacks. For large institutions and mainstream users, Coinbase is often the preferred—or even sole—choice. For example, in the U.S., many traditional funds can only use licensed exchanges due to regulatory constraints, giving Coinbase a natural market share. Furthermore, Coinbase proactively cooperates with regulators (KYC/AML compliance, etc.), earning a strong reputation among policymakers and lobbying for favorable regulations. The barriers created by brand trust and compliance are difficult for new entrants to replicate quickly or at low cost. License applications typically take 12–18 months and require ongoing capital adequacy, anti-money laundering, cybersecurity audits, and other annual reviews; for a new platform to obtain licenses in all states could require hundreds of millions of dollars in compliance costs. Even if a new entrant is technologically competitive, without regulatory backing and years of incident-free operation, it is difficult to challenge Coinbase’s position among conservative funds and novice users in the short term. This trust advantage also allows Coinbase to command a premium: users are willing to pay relatively higher fees for a secure and reliable platform.

Network Effects and Liquidity

Exchange businesses exhibit clear network effects: more users and trading volume generate deeper liquidity and a better trading experience, which in turn attracts even more users. After years of operation, Coinbase has accumulated a large global user base and massive trading volume. Statistics show that 67% of cryptocurrency holders in the U.S. have used Coinbase. This high coverage makes Coinbase a “gateway” platform in the crypto space; new tokens and projects often aim to list on Coinbase to reach a broad audience. A large user base also ensures deep order books and tight bid-ask spreads, which are crucial for trading experience. Particularly during periods of high price volatility, platforms with deep liquidity can better handle large trades without significant slippage, further reinforcing professional traders’ reliance on Coinbase. Network effects are also amplified through word-of-mouth: the more users there are, the stronger the referral effect, and beginners tend to choose platforms that their friends use, creating a positive feedback loop. It is very difficult for competitors to break this cycle unless they offer extremely differentiated services in a niche market (e.g., zero fees or support for unique assets). Currently, Coinbase’s network effects in the U.S. and European markets are relatively solid.

Economies of Scale & Multi-Product Stickiness

Coinbase’s scale advantages are reflected not only in network liquidity effects but also in cost efficiency and business diversification. As a publicly listed company, Coinbase can raise sufficient capital to invest in system security, product development, and compliance teams, which lowers costs per unit of transaction. Smaller platforms often cannot afford such expensive compliance and security investments. Coinbase’s operational efficiency improves as its user base grows, creating an economies-of-scale moat. At the same time, Coinbase’s diversified business segments—trading, custody, staking, stablecoins, etc.—reinforce user stickiness. Users do more than just trade on Coinbase: they hold coins to earn interest, participate in staking to earn rewards, and use USDC for payments. Meeting multiple needs on a single platform increases switching costs, further strengthening user loyalty.

Technology & Security Moat

Although the technological barriers in trading are not as high as in some advanced tech industries, Coinbase has built a certain tech moat over years in areas such as high-concurrency matching engines, wallet security, and multi-chain support. Its trading engine has been tested during peak bull markets (e.g., daily trading volumes of hundreds of billions in 2021) and demonstrates stability under extreme trading surges. In terms of wallet security, Coinbase has never experienced a major hack, a record many competitors cannot claim—even Binance has suffered losses in the hundreds of millions. Additionally, Coinbase has developed many proprietary internal systems, including tools for monitoring suspicious transactions, preventing market manipulation, and providing professional APIs for institutional clients and partners. These systems are not easily replicable in the short term. Particularly in security and risk management, even a single major vulnerability could severely damage a new platform’s reputation, whereas Coinbase’s years of security investment have built strong user trust as a barrier to entry.

Sustainability of the Moat Can these moats be maintained long-term? Let’s evaluate each:

Brand & Compliance: With more mainstream institutions entering crypto and regulatory frameworks becoming clearer, Coinbase’s accumulated licenses will become increasingly valuable. Its first-mover advantage is likely to expand, as it has established a hard-to-challenge reputation and enjoys experience and scale benefits in licensing and compliance. However, regulatory uncertainty remains a potential risk—for example, changes in government or Congress could shift U.S. crypto regulations, potentially limiting Coinbase’s core market.

Network Effects: These are likely stable as long as Coinbase avoids trust crises or prolonged technical failures. Users are unlikely to migrate easily. Yet, the rise of decentralized finance (DeFi) may weaken network effects among some professional users (e.g., moving to Uniswap or on-chain platforms like Hyperliquid). Currently, DeFi’s user experience and liquidity are insufficient to significantly challenge Coinbase. Moreover, Coinbase’s development of Base and smart crypto wallets helps hedge against this trend.

Economies of Scale & Multi-Product Stickiness: These advantages become more pronounced as the company grows. Larger scale improves cost structure and raises user ARPU, creating a positive feedback loop. Risks exist, however: expanding business lines could dilute management focus, and regulatory requirements across products are complex, requiring careful oversight.

Technology Barrier: Maintaining this moat requires ongoing investment. Coinbase spends heavily on R&D (e.g., $1.2B in 2023, ~40% of revenue; $1.32B in 2024, absolute value up 11%, revenue proportion down to 22%). Sustaining this level of investment should preserve technological leadership.

Overall Assessment: Coinbase has established a significant moat, particularly in the U.S., with a unique advantage in trust and compliance branding. As the industry matures, the “strong get stronger” effect may concentrate capital and users toward leading compliant platforms, further deepening Coinbase’s moat. Unless a major disruptive shift occurs (e.g., DeFi fully replacing centralized exchanges, or Coinbase suffers a major failure), its competitive advantages are expected to persist in the foreseeable future.

8. Key Risks & Challenges

Coinbase still faces several critical risk factors:

Macro & Industry Cycle Risks The cryptocurrency market is highly cyclical, and Coinbase’s performance is heavily dependent on trading volume and coin prices. During bear markets like those in 2018 and 2022, trading activity can shrink sharply, putting pressure on the company’s revenue and profits, and potentially causing losses again. Macro tightening—such, such as reduced liquidity or high interest rates—can also dampen market speculation and asset prices. Additionally, the crypto market remains immature and sensitive to single events (exchange bankruptcies, hacks, large sell-offs, etc.), which can trigger widespread confidence declines. For example, the 2022 FTX collapse caused a sharp drop in industry-wide trading volumes; although Coinbase was not directly exposed, its overall business was still affected.

Regulatory Uncertainty Regulation remains one of the greatest uncertainties for Coinbase, especially in the U.S. The SEC and other agencies have yet to provide clear guidance on which tokens are classified as securities or whether exchanges violate regulations by offering certain services (though the situation has improved recently). Moreover, the U.S. has not yet enacted comprehensive digital asset trading laws; the passage of the Clarity Act this year is uncertain, and if delayed into next year, midterm elections could add further unpredictability. Internationally, regulatory changes in other countries may also affect Coinbase’s overseas expansion plans.

Technology, Security & System Stability Risks As a platform holding hundreds of billions in user assets, Coinbase faces significant cybersecurity and operational risks. Any hack resulting in customer asset theft would severely damage its reputation and financial position. The crypto industry frequently experiences hacks, and even with Coinbase’s strong track record, vigilance is essential. In addition, system crashes or outages during high-concurrency trading periods pose risks. Historically, Coinbase has experienced brief outages during volatile market periods, which drew user complaints; if the platform cannot facilitate trades at critical times, users may migrate elsewhere. New products (e.g., smart contracts) may contain code vulnerabilities, and staking or other services carry protocol risks, all of which require careful management.

Compliance Costs & Legal Risk As regulation strengthens and standards clarify, the path to compliant operations becomes clearer, but compliance costs may rise correspondingly. Maintaining licenses in multiple jurisdictions, AML monitoring, personnel verification, and other obligations represent significant annual expenses. Increased regulatory scrutiny can also distract management. If future laws impose additional obligations (e.g., trade reporting, user asset capital requirements), operational burdens and profitability could be affected. As an industry benchmark, Coinbase is also a likely target for litigation, including class actions and user disputes. Lawsuits not only entail compensation costs but can also damage the brand. For example, in 2022 some users sued Coinbase over allegedly misleading promotions; although the amounts were small, they consumed company resources. Legal disputes may continue to arise, requiring a strong legal team (currently led by a capable CLO), but legal and reputational risks cannot be entirely eliminated.

Intensifying Market Competition Although Coinbase currently holds a strong position, the competitive landscape evolves rapidly. Major competitors like Binance continue to exert pressure in certain markets (lower fees, more tokens). If Binance resolves regulatory challenges, its large user base could threaten Coinbase’s global market share.

- Traditional financial giants may also enter: for instance, Intercontinental Exchange (ICE) acquired U.S. crypto exchange Bakkt, and Nasdaq has relevant initiatives. Large investment banks or tech companies could launch their own crypto trading platforms, leveraging resources and capital to capture customers.

- Innovative models: The rise of decentralized exchanges (DEX) and DeFi poses long-term challenges to centralized platforms. While DEX experiences are currently limited, technical progress is ongoing, and some sophisticated users have shifted to self-custody trading. If DEX platforms surpass centralized exchanges in performance and liquidity over the next few years, Coinbase could lose high-end users. Fintech brokers (e.g., Robinhood) expanding crypto support also capture some retail flow.

M&A & Integration Risks Coinbase has expanded through acquisitions and new business ventures, such as the NFT platform and various startups. Integration risks include cultural fit, technical alignment, and unmet expectations. The NFT business is an example where acquisition teams and internal resources failed to synergize effectively. Future acquisitions (e.g., payment companies, custodial firms) may carry similar risks, including underperformance or diluted focus on core operations. Large-scale M&A also involves regulatory approval risks; as a market leader, any industry acquisition may face antitrust scrutiny (e.g., acquiring another U.S. exchange could be blocked).

Global Geopolitical & Legal Environment Risks As a multinational, Coinbase faces risks from political and economic changes in different countries. Some jurisdictions could suddenly ban crypto trading, or international sanctions (e.g., restrictions on Russian users during the Russia-Ukraine conflict) could create complex compliance requirements. Exchange rate and tax policy changes could also impact international business profits. While not core risks, these require the company to maintain global contingency capabilities.

Summary: Among these risks, regulatory uncertainty and market cycles are the most significant and will continue to materially affect Coinbase’s future performance. The company has taken measures to address these challenges, but substantial uncertainty remains.

9. Valuation

We value Coinbase using a relative valuation approach and consider both bull and bear scenarios to estimate a target price range.

Valuation Method:

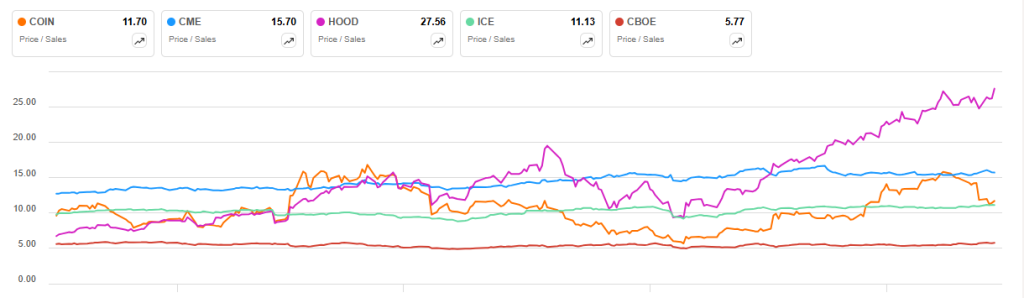

- Price-to-Sales (P/S) Ratio: Given Coinbase’s highly volatile performance, using earnings-based metrics such as P/E is unstable, making the P/S ratio a more intuitive measure. Historically, Coinbase has traded near 20x P/S during peak periods, while in bear markets it fell below 3x P/S. Currently, the stock price corresponds to a trailing twelve-month revenue P/S of approximately 11.7x (this high multiple reflects investor expectations for continued rapid revenue growth). Compared with most other trading-platform fintech companies, this multiple is moderate, particularly well below that of peer Robinhood. Considering Coinbase’s high gross margin and strong growth leverage, a base-case P/S range of 10–15x is reasonable, implying a market capitalization of $67.1–100.7 billion and a share price of $232–348 (based on a fully diluted share count of 2.89 billion, for conservatism).

- Enterprise Value / EBITDA (EV/EBITDA): Traditional exchanges are often valued based on EBITDA. Coinbase’s current EBITDA (TTM) is approximately $3.18 B, corresponding to an EV/EBITDA of about 24×. This is slightly higher than exchanges like CME and CBOE, which trade around 18–22×, but well below Robinhood at 63×. Compared with traditional trading platforms, Coinbase has higher growth potential but also greater earnings volatility, leading to a lower discounted value. Under baseline assumptions regarding regulatory environment and industry development, a reasonable EV/EBITDA range for Coinbase could be 20–30×, corresponding to an equity value (EV) of roughly $63.6–95.4 B and a share price of $220–330. To maintain a sufficient margin of safety, one could apply a 20–30% discount to this EV/EBITDA range as a potential buying range (similarly for P/S).

10. Conclusion

Summary: As a leading global platform for crypto asset trading and services, Coinbase possesses strong potential for sustained growth in the crypto finance wave, supported by its brand trust, broad user base, and diversified product offerings. The company has experienced both rapid growth and sharp pullbacks in recent years, but management has actively responded, maintaining financial stability and strategic discipline. Coinbase’s long-term value is underpinned by the following factors:

- Strong reputation in compliance and security: This helps attract mainstream and institutional capital consistently.