Contents

Preface

Having witnessed the volatility of crypto markets, from the bullish surge of 2020 to the bearish grind of 2023, we’ve come to realize that within the Web3 business world, the bedrock of established business models is found firmly within the domain of DeFi. Central to this ecosystem are decentralized exchanges (DEXs), lending protocols, and stablecoins, with derivatives also gaining considerable traction in the space. Notably, these sectors have exhibited a remarkable degree of resilience even amidst a bear market.

At Mint Ventures, our analysis has deeply delved into the intricacies of DEXs and stablecoins, covering a wide array of ve(3,3) projects such as Curve, Trader Joe, Syncswap, iZUMi, and Velodrome, as well as stablecoin ventures including MakerDao, Frax, Terra, Liquity, Angle, Celo, and others. In this latest edition of Clips, we pivot our focus to the lending protocols, casting a spotlight on the new player Morpho, which has seen rapid growth in business metrics over the past year.

This clip will navigate through the operational fabric and strategic expansions of Morpho, alongside its freshly introduced lending infrastructure, Morpho Blue. Our inquiry will navigate through the intricacies of the current DeFi lending market, Morpho’s innovative approach to decentralized credit, and the potential market shake-up instigated by Morpho Blue.

- How does the present landscape of the DeFi lending sphere appear?

- What operational facets does Morpho encompass, which market inefficiencies is it addressing, and what progress has it charted in its business voyage?

- What are the prospects for the newly launched Morpho Blue? Could it challenge the leading positions of Aave and Compound and what broader impacts could we anticipate?

The insights offered herein represent a snapshot of my analysis, framed by the knowledge available at the time of writing. There may be factual inaccuracies or biases. This article is intended for discussion purposes only, and feedback is welcomed.

The Landscape of Decentralized Lending Protocols

Organic Demand Rises as Mainstream Focus, Eclipsing Ponzi-Like Models

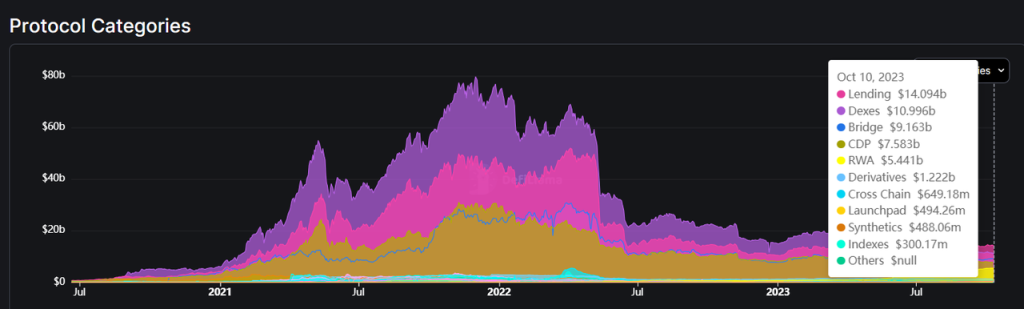

Decentralized lending has consistently ranked at the forefront regarding capital capacity, with its Total Value Locked (TVL) now surpassing that of decentralized exchanges (Dex), becoming the premier avenue for capital allocation within the DeFi sector.

Decentralized lending is also one of the rare categories in the Web3 domain that has achieved “Product-Market Fit” (PMF). Despite the ‘DeFi summer’ phenomenon between 2020 and 2021, where many projects aggressively fueled lending activities with token incentives, such practices have waned in the wake of a bearish market turn.

In the decentralized finance realm, Aave, a vanguard in the lending protocol sector, has charted a course of robust fiscal performance. Data delineated below underscores a pivotal trend: Aave’s protocol revenue has consistently eclipsed its token incentive expenditures since December 2022. A September snapshot reveals protocol earnings reaching $1.6 million, towering over the relatively modest sum of $230,000 in token incentives. Moreover, Aave’s token incentives are mainly aimed at bolstering the staking of $AAVE as a safety module to secure the protocol against bad debt and to compensate for the treasury when it falls short, rather than incentivizing deposit and borrowing behaviors. Consequently, Aave’s deposit and borrowing activities are enjoying a period of ‘organic’ growth, not sustained by liquidity mining drives that can often echo the unsustainable mechanics of Ponzi frameworks.

Source: https://tokenterminal.com/

Parallel strides are evident within Venus, a heavyweight lending protocol within the BNBchain ecosystem, which has also seen its protocol revenue surpass its incentive expenditures since March 2023. This shift marks a transition towards a more healthy operational framework, weaning off the need for aggressive deposit and borrowing incentives.

Source: https://tokenterminal.com/

However, many lending protocols continue to rely heavily on token subsidies to fuel supply and demand within their ecosystems, where the value of the incentives provided for lending activities far exceeds the revenue they can generate.

For instance, Compound V3 continues to provide $COMP token subsidies for deposit and borrowing activities.

Source: https://app.compound.finance/markets/weth-mainnet

Source: https://app.compound.finance/markets/weth-basemainnet

If Compound relies heavily on token subsidies to maintain its market share, then another protocol, Radiant, could be described as a purely Ponzi structure.

Delving into the lending market page on Radiant’s platform, two aberrant phenomena are immediately conspicuous:

Firstly, there is a significant disparity in borrow APY when compared to traditional market standards. Whereas typical borrow APY for stablecoins is generally within the 3-5% range, Radiant’s borrowing rates are markedly elevated, averaging between 14-15%. This trend extends to other assets within Radiant’s ecosystem, where the borrow APYs are observed to be as much as 8-10 times higher than those in mainstream protocols.

Secondly, Radiant’s platform strategy prominently features the promotion of ‘looping loans’. This mechanism allows users to deposit a single type of asset as collateral, subsequently engaging in a continuous cycle of depositing and borrowing. The primary objective of this strategy is to artificially inflate the user’s total deposit-borrow volume. This, in turn, maximizes the mining incentives accrued in Radiant’s native token, $RDNT. In essence, this approach could be interpreted as an indirect method employed by the Radiant team to distribute RDNT tokens to its users, in exchange for the fees collected on borrowings.

At the heart of Radiant’s economic model lies a critical issue: the primary driver of its fee generation is not the authentic lending activity but rather the pursuit of RDNT tokens. This creates a precarious economic structure that resembles a Ponzi scheme, where the system is essentially self-feeding. In this environment, there aren’t genuine financial consumers engaging in lending practices. The practice of loop loans, where a user acts as both depositor and borrower of the same asset, further complicates the scenario. This model is inherently flawed as it creates an economic cycle where the source of RDNT dividends is the user themselves, lacking any external or organic financial input. In this structure, the only entity assured of risk-free profits is the platform operator, which garners gains from transaction fees, appropriating 15% of the interest income. While the Radiant project team has temporarily mitigated the immediate risks of a financial implosion – typically associated with a drop in the price of $RDNT – through the implementation of the dLP staking mechanism, the long-term viability of this model remains in question. Unless there is a strategic pivot from this Ponzi scheme to a more sustainable business model, the potential for a systemic collapse – a ‘death spiral’ – remains a significant concern.

However, in the broader decentralized lending market, exemplified by leading projects like Aave, there’s a discernible shift away from heavy reliance on subsidies to sustain operational revenues. Instead, there’s a move towards more sustainable and healthier business practices.

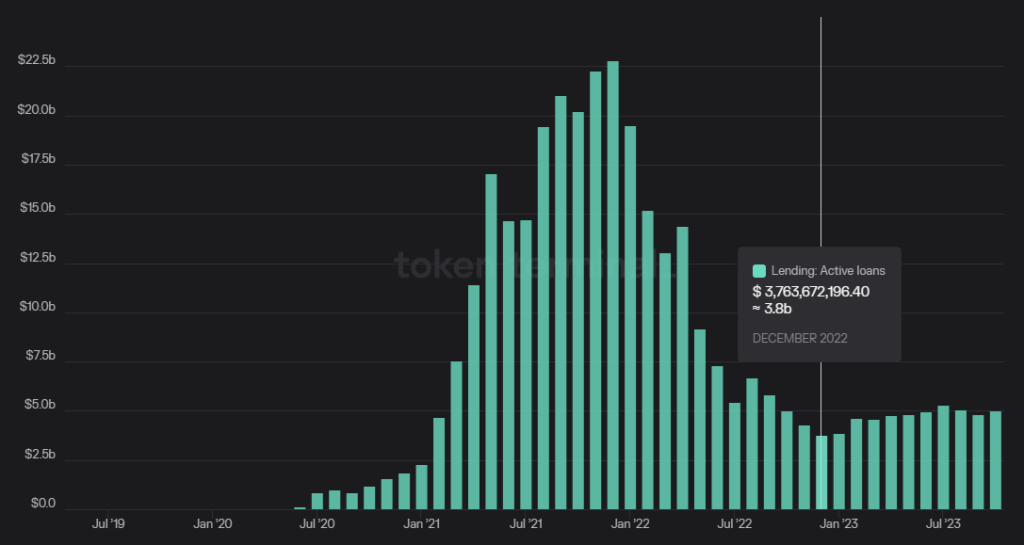

The following graph shows the active loan volume in the Web3 lending market from May 2019 to October 2023. Starting from a modest base in the hundreds of thousands, the market peaked at $22.5 billion in November 2021, experienced a downturn to $3.8 billion in November 2022, and is currently valued at around $5 billion. This trend indicates a gradual recovery from its lowest point, showcasing remarkable resilience and business adaptability within the sector, even amid challenging market conditions.

Defined Competitive Edges and Elevated Market Concentration

As the infrastructures of DeFi, compared to the DEX market, which exhibits a more competitive landscape, a cornerstone of DeFi, the lending sector benefits from stronger competitive moats, a fact that becomes evident when considering several key factors:

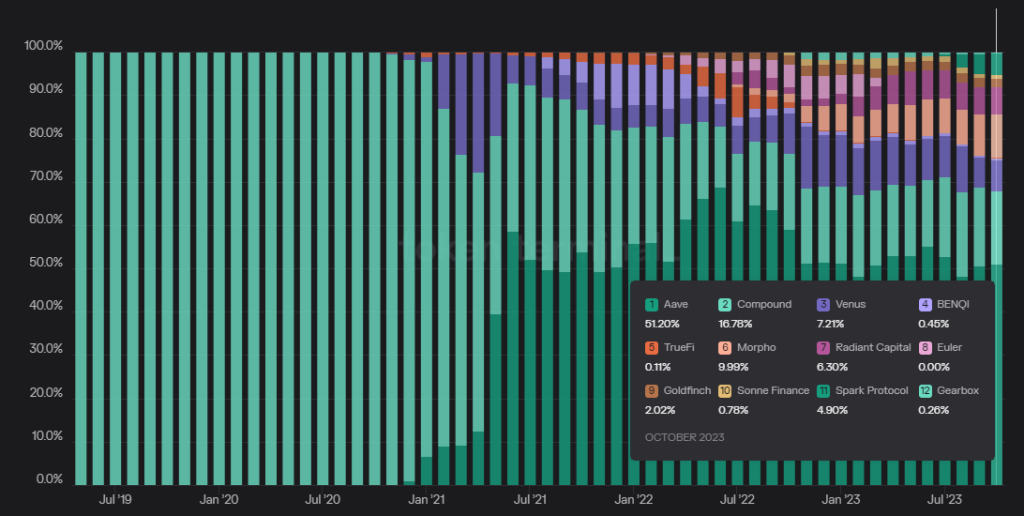

1. Stability in Market Share: The chart below demonstrates the review of the active borrowing volumes among lending protocols, calculated as a percentage of total market share from May 2019 to October 2023. Since mid-2021, post an intensified push by Aave, its market share has consistently hovered within the 50-60% bracket, showcasing remarkable stability and resilience. Compound, despite experiencing a compression in its market share, continues to maintain a robust and stable position.

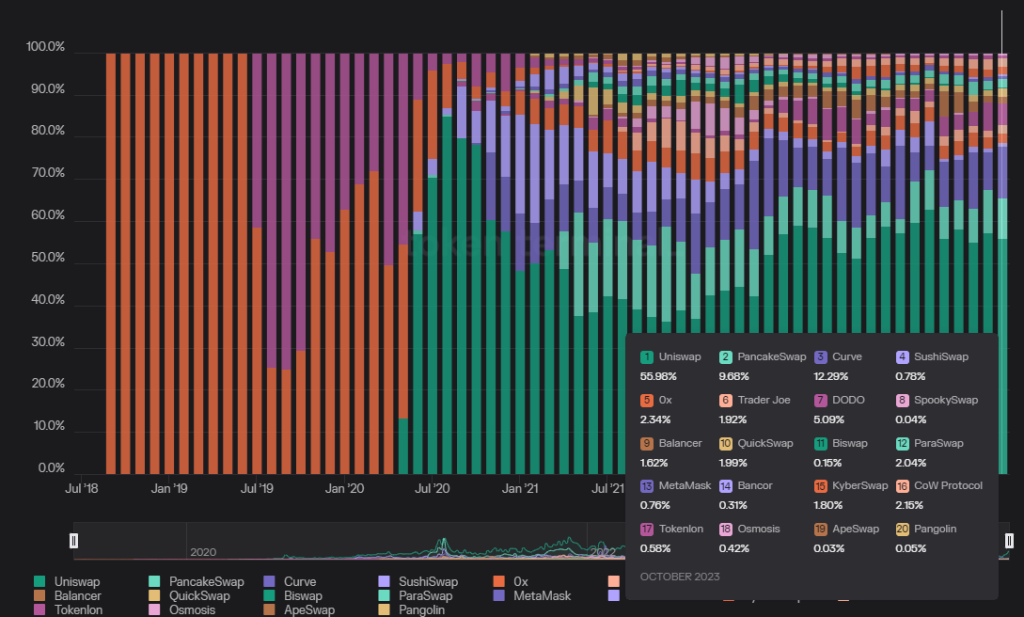

In stark contrast, the Dex sector has experienced more volatile shifts in market share. Uniswap, following its introduction, swiftly clinched nearly 90% of the trading volume market share. Nonetheless, this dominance was challenged by the rapid ascent of platforms like Sushiswap, Curve, and Pancakeswap. This competition eroded Uniswap’s hold, reducing its share to approximately 37% at one point, although it has since recovered to about 55%. Furthermore, the Dex sector is characterized by a significantly larger number of active projects compared to the lending space.

2. Enhanced Profitability in Lending Projects: As mentioned in the previous section, projects like Aave have managed to generate positive cash flow without resorting to subsidizing borrowing activities. reporting consistent monthly interest spread revenues in the range of approximately $1.5-2 million. This contrasts sharply with the scenario in most Dex projects. For instance, Uniswap, despite its market prominence, hasn’t activated protocol-level fees (only frontend fees are active), and many Dex projects are operating at an effective loss, where the cost of token emissions for liquidity incentives outweighs the revenue generated from protocol fees.

The competitive edges around top lending protocols can be broadly attributed to their brand strength in terms of security, which can be further broken down into two points:

- Long History of Secure Operations: Since the DeFi Summer of 2020, there’s been a proliferation of fork projects inspired by Aave or Compound across various blockchain networks. However, many of these new entrants have encountered security attacks or substantial bad debt losses soon after their launch. In contrast, Aave and Compound have maintained a clean track record, free from significant attacks or insurmountable bad debt incidents. This history of safe, reliable operation in a real-world network environment serves as a vital assurance of security for depositors. Newer lending protocols, even those offering potentially more innovative features and higher short-term APYs, struggle to win user trust, particularly from large-scale investors (whales), in the absence of a proven, long-term operational record.

- Sufficient security budgets: The top lending protocols, thanks to their higher commercial revenues and more substantial treasury funds, are able to allocate significant resources for security audits and asset risk control. This is crucial both for the development of new features and the introduction of new assets.

In summary, the lending market has demonstrated organic demand and a sustainable business model, characterized by a relatively concentrated market share.

Morpho’s Business and Operational Status

The Interest Rate Optimizer

Morpho is a peer-to-peer lending protocol, also known as lending pool optimizer, built on top of Aave and Compound. It is designed to address the issue of inefficient capital utilization in pool-to-peer lending protocols like Aave, there is often a mismatch between the total funds deposited and the total funds borrowed.

The value proposition of Morpho is straightforward and impactful.: to provide enhanced interest rates for both lenders and borrowers. This means higher returns on deposits and lower interest rates for loans.

The inefficiency in capital utilization within pool-to-peer lending models, as employed by platforms like Aave and Compound, lies in the inherent mechanism of these models, where the total volume of deposited funds (the pool) consistently exceeds the total volume of loaned funds (the point). Typically, a scenario may present itself where there’s a total of 1 billion $USDT in deposits within the currency market, but only 600 million $USDT is lent out.

For depositors, this scenario means that their returns are diluted. Although the idle 400 million USDT is not directly loaned out, it still forms part of the pool generating interest from the 600 million USDT that is actively loaned. Consequently, the interest accrued is distributed across the entire 1 billion USDT deposited, leading to lower earnings per depositor. On the flip side, despite utilizing only a fraction of the total pool, borrowers are subjected to interest costs as if they were borrowing against the entire pool’s funds. This results in a higher interest burden per borrower and the mismatch between deposited and borrowed funds.

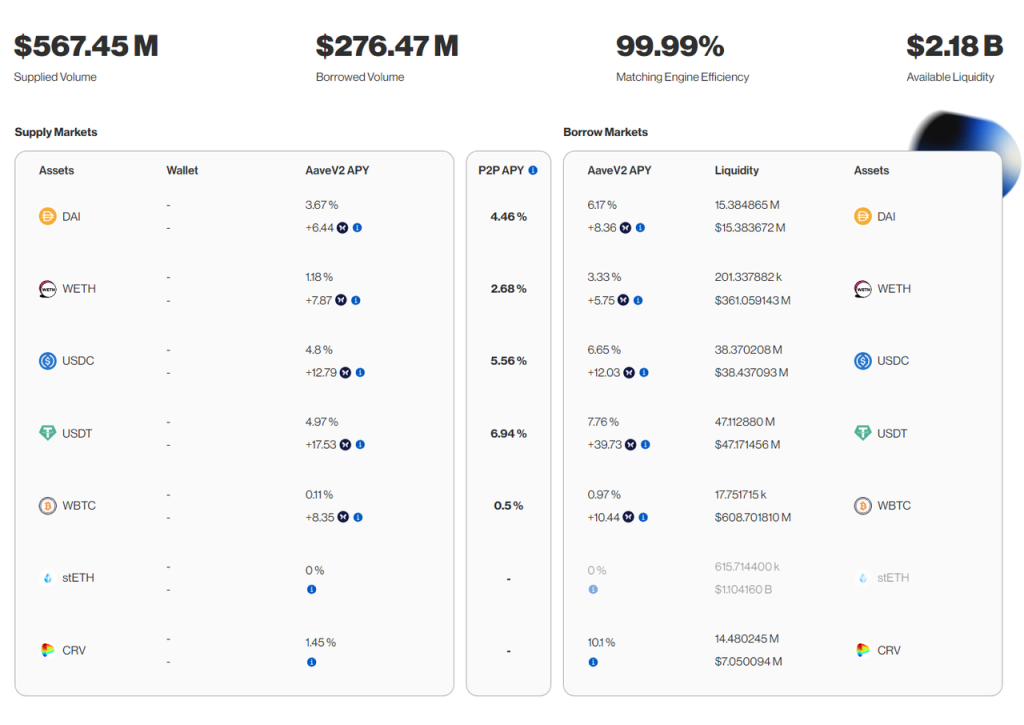

Let’s take the rate optimizer module on top of Aave V2, which currently has the largest volume of Morpho’s deposit business, as an example of how Morpho’s rate optimization service addresses capital inefficiency.

- Deposit: Bob opts to deposit 10,000 DAI into Morpho. Morpho then places these funds into the Aave V2 market. At this point, the deposit interest rate provided by the Aave platform for DAI is 3.67%.

- Borrowing and Collateral: On the other side, Alice intends to borrow 10,000 DAI. To facilitate this, she deposits 20 ETH as collateral into Morpho. Morpho secures Alice’s collateral in the Aave V2 market, mirroring the process it uses for handling deposits.

- Loan Matching: Morpho redeems the 10,000 DAI previously deposited by Bob in Aave and directly lends it to Alice. This direct matching means Bob’s deposit is fully utilized without any idle funds. For Alice, the benefit is that she is liable for interest only on the actual amount of DAI borrowed, not on the total pool volume. As a result of this direct peer-to-peer (P2P) lending mechanism, both parties enjoy optimized rates: Bob Earns a higher deposit APY of 4.46%, compared to the Aave pool APY of 3.67%, Alice Benefits from a lower borrowing APY of 4.46%, as opposed to Aave’s pool APY of 6.17%.

Note: In this scenario, the specific Peer-to-Peer APY of 4.46% and whether it is closer to the lower limit (deposit APY) or upper limit (borrow APY), is determined by Morpho’s internal parameters. These parameters are controlled by the community governance.

- Solving Liquidity Mismatches: Consider a scenario where Bob, having deposited 10,000 DAI, decides to withdraw his funds. However, at this moment, Alice, who borrowed these funds, hasn’t repaid her loan yet. In this case, if no other depositors are available to match, Morpho uses the 20 ETH Alice deposited as collateral to borrow the equivalent amount (principal plus accrued interest, over 10,000 DAI) from Aave. This action allows Bob to successfully withdraw his deposit.

- Matching Order: Morpho’s operational protocol regarding the matching of funds follows a “larger funds first serve” principle. This approach means that the platform gives priority to matching larger deposits and borrows before smaller ones. The underlying rationale for this strategy is to keep the proportion of gas costs to the total transaction value low. If the gas cost required to execute a match is disproportionately high relative to the amount being matched, the system will not proceed with the match.

The essence of Morpho’s business model is its innovative approach to using the existing capital pools of Aave and Compound as foundational elements. By acting as a rate optimization service, Morpho effectively matches depositors and borrowers.

The ingenuity of this model lies in leveraging the composability of the DeFi ecosystem, showcasing how Morpho has effectively attracted user funds in a way that can be likened to “making something out of nothing.” This approach is particularly appealing to users for several reasons:

- At a basic level, users on Morpho are guaranteed to earn returns or incur borrowing costs equivalent to those on Aave and Compound. However, when Morpho successfully matches depositors and borrowers directly, it leads to higher returns for depositors and lower costs for borrowers.

- Morpho’s product architecture, built atop Aave and Compound, also replicates the risk parameters of these platforms. By allocating funds within Aave and Compound, Morpho inherits not just the operational mechanics but also the brand reputation of these two protocols.

The effectiveness of Morpho’s design and its clear value proposition have been reflected in its remarkable growth. Within just over a year of its launch, Morpho has managed to accumulate nearly $1,000,000,000 in deposits, ranking just behind giants like Aave and Compound in terms of deposit volumes.

Business Metrics and Tokenomics

Business Metrics

The following chart illustrates Morpho’s total supply volume (blue line), total borrow volume (light brown line), and matched amounts (dark brown).

These metrics collectively paint a picture of the continuous growth in all business scales of Morpho. The deposit matching rate stands at 33.4% and the borrow fund matching rate reaches 63.9, which are quite impressive figures.

Tokenomics

Morpho has a total token supply capped at 1 billion tokens, with 51% of the total token supply allocated to the community, 19% of the token sold to investors, 24% of the token supply is held by the founders, the development company Morpho Labs, and the operating entity, Morpho Association, the remaining percentage is earmarked for advisors and contributors.

The Morpho token, though already issued and being utilized for governance voting and project incentives, is in a non-transferable state. Consequently, it does not have a secondary market price. This means that token holders can engage in governance decisions but are unable to sell their holdings.

Unlike some projects that have a predefined structure for token distribution and incentives (like Curve), Morpho’s approach to token incentives is more dynamic and flexible. Incentives are determined on a quarterly or monthly basis, allowing the governance team to adjust the intensity and strategies of these incentives in response to market conditions.

This pragmatic and flexible method of token incentive distribution might become a more mainstream model in the Web3 business world.

Morpho’s approach to incentives is comprehensive, targeting both deposit and borrowing behaviors. Over the past year, Morpho has distributed 30.8 million tokens for incentives, which is about 3.08% of the total token supply. This may seem like a modest proportion. Moreover, as indicated in the graph below, Morpho’s official token expenditure shows a trend of decreasing spending on incentives. Interestingly, this reduction has not negatively impacted the growth rate of Morpho’s operations.

This transition is a positive signal for the platform, indicating that Morpho has a sufficiently full Product-Market Fit (PMF), with user demand becoming increasingly organic. With 51% of the community token share still having approximately 48% remaining, Morpho retains a substantial budget and allows flexibility and room for strategic allocation in future growth phases or new market ventures.

Despite this, Morpho has not yet started charging for its services.

Team and Financing

The core team of Morpho originates from France, primarily located in Paris. The key team members have been publicly identified, and the three founders have their roots in the telecommunications and computer industries, boasting rich backgrounds in blockchain entrepreneurship and development.

Morpho has completed two rounds of funding to date: a $1.3 million seed round in October 2021 and an $18 million Series A round in July 2022, led by investors A16z, Nascent, and Variant.

If the aforementioned financing amounts correspond to the officially disclosed 19% investor share, it can be inferred that the total valuation of the project stands at around $100 million.

Morpho Blue and Its Potential Influence

What is Morpho Blue?

Put simply, Morpho Blue acts as a permissionless lending protocol layer. This sets it apart from platforms like Aave and Compound, as it opens up a broader spectrum of lending possibilities. Anyone can use Morpho Blue to create their own lending market based on it. The dimensions available for builders to choose from include:

- Asset Collateralization Options

- Choice of Assets to Lend Out

- Oracle Selection for Price Feeds

- Determining Loan-to-Value(LTV) and Liquidation Loan-to-Value(LLTV) ratios

- Implementing an Interest Rate Model(IRM)

What value will Morpho Blue bring?

As outlined in its official documentation, the characteristics can be summarized as follows:

- Trustless

- Morpho Blue is designed to be immutable. It means once its code is deployed, it cannot be modified, reflecting a commitment to minimal governance.

- With just 650 lines of Solidity code, Morpho Blue stands out for its simplicity and security.

- Efficient

- Users have the flexibility to choose higher Loan-to-Value (LTV) ratios and more favorable interest rates.

- Morpho Blue sidesteps the need to pay fees for third-party audit and risk management services.

- Employing a singleton smart contract with a simple code structure, Morpho Blue significantly cuts down on gas costs, achieving a reduction of about 70%.

*Note: A singleton smart contract refers to a protocol using a single contract for execution, rather than a combination of multiple contracts. Uniswap V4 also adopted a singleton contract approach.

- Flexible

- In Morpho Blue, both market building and risk management aspects, including oracles and lending parameters, are permissionless. This deviates from the uniform model adopted by platforms like Aave and Compound, where the entire platform adheres to a standard set of protocols and rules governed by a DAO.

- Morpho Blue is tailored to be developer-friendly, integrating a range of contemporary smart contract patterns. It offers account management features that facilitate gasless interactions and account abstraction. Additionally, the platform provides free flash loans, enabling users to access assets across all its markets in a single call, with the condition that the loan is repaid within the same transaction.

Morpho Blue employs a product philosophy akin to that of Uniswap V4, positioning itself as a foundational layer for a wide array of financial services. This approach involves opening up the modules above this foundational layer, thereby enabling various parties to come in and offer their distinct services.

Morpho Blue’s approach differs from Aave in a key aspect: while Aave’s lending and borrowing processes are permissionless, the decisions regarding which assets can be borrowed or lent, the nature of risk control rules (whether conservative or aggressive), the selection of oracles, and the setting of interest and liquidation parameters, are all governed and managed by the Aave DAO and the various service providers like Gauntlet and Chaos, who monitor and manage over 600 risk parameters on a daily basis.

Morpho Blue functions more like an open lending operating system. It allows users to construct their own optimal lending combinations on its platform, much like they would on Aave. Additionally, professional risk management firms such as Gauntlet and Chaos have the opportunity to seek partnerships in the market, providing their risk management expertise to others and earning corresponding fees.

From my perspective, the fundamental value proposition of Morpho Blue lies not just in its trustlessness, efficiency, or flexibility, but primarily in its establishment of a free market for lending. This platform enables collaboration among all participants in the lending market, thus offering a more diverse and enriched array of market options for clients at every stage of their lending journey.

Will Morpho Blue Pose a Threat to Aave?

Possibly.

Morpho stands distinct among the myriad competitors that have emerged to challenge Aave, having accrued multiple advantages over the past year:

- Morpho, with its managed capital hitting the $1 billion mark, is fast approaching the league of Aave, which oversees a substantial $7 billion in capital management. While these funds are presently employed within the Morpho Interest Rate Optimizer, there are many ways to channel them into new features and functionalities.

- Morpho, recognized as the quickest expanding lending protocol in the past year and with its token still awaiting official release, presents a realm of possibilities. The introduction of major new features by Morpho could readily captivate user interest and drive participation.

- Morpho boasts a substantial and adaptable token budget, well-equipped to entice early-stage users through attractive subsidy offerings.

- Morpho’s consistent operational track record, coupled with its significant fund volume, has enabled it to establish a notable degree of security branding.

This doesn’t automatically put Aave on a back foot in upcoming competitive landscapes. Many users might not have the bandwidth or interest to sift through a plethora of lending choices. The lending solutions curated under the centralized governance of the Aave DAO might still hold the upper hand, continuing to be the go-to choice for the majority of users.

Second, Morpho Rate Optimizer largely inherits the security credentials of Aave and Compound, which has gradually put more money at ease. However, Morpho Blue, as a distinct and novel product featuring its own codebase, may initially encounter cautiousness from whales – to take a beat before diving in with full trust. This cautious approach is understandable, given the still-lingering sting from security mishaps in earlier permissionless lending markets like Euler, which remain top of mind in the crypto community.

Furthermore, Aave is fully capable of developing a set of functions similar to the Morpho Rate Optimizer on its existing framework to meet user demands for increased capital matching efficiency, potentially pushing Morpho out of the P2P lending market. However, that possibility seems unlikely at the moment, given that Aave also issued Grants to NillaConnect, a Morpho-like P2P lending product, this past July, instead of creating their own.

Lastly, the lending business model adopted by Morpho Blue doesn’t markedly diverge from the existing paradigms set by Aave. Aave is also capable to observe, monitor, and potentially replicate any effective lending mechanisms that Morpho Blue demonstrates.

But in any case, the launch of Morpho Blue is set to introduce an open lending testbed, paving the way for inclusive participation and combination opportunity across the full spectrum of the lending process. Could these newly interconnected lending collectives emerging from Morpho Blue spearhead a solution that stands a chance against Aave?

We will see what happens.