Contents

Key Insights

This is a report on Tokemak’s initial research. As Tokemak has not yet launched its staple and research documentation, the report involves less data analysis and will focus on economic model analysis, supplemented by industry comparison and data analysis.

Tokemak has issued its native protocol token, Toke.

Core Investment Logic

Market Demands

There is a strong and rapidly growing demand for liquidity in the market, forming a long-term and stable demand.

Innovation Mechanism

Despite the plethora of liquidity mining projects at the moment, market liquidity remains scarce. Tokemak, a novel liquidity management system, promises to act as a new liquidity router in the liquidity mining track and become the next generation of liquidity management infrastructure.

Tokemak has the following advantages over similar platforms:

- Liquidity Providers allow for single-asset mining and do not need to bear the risk of impermanent loss (except in extreme cases)

- Liquidity Demanders (project owners or DEX that need to build token liquidity) have access to sustainable liquidity and the ability to manage token liquidity across exchanges

- Tokemak automatically optimizes liquidity allocation

Multi-dimensional Support

Driven by Framework Ventures, ConsenSys, and Coinbase Ventures to solve cold-start problems in the early stage.

Main Risks

Product Mechanism Risks

- Even though Tokenmak has disclosed their innovation, the main product has not been launched yet, and its business logic needs to be tested by market and time.

- As liquidity miners currently prefer high-risk investments, it remains to be verified whether liquidity supply with low risk preference is in great demand.

- It is both an innovation and a risk that the risk of impermanent loss is transferred from the Liquidity Provider to the liquidity demander and the platform itself. Providing safety for Liquidity Providers exposes the platform to more downside risks.

Smart Contract Risks

The large amount of original codes and functions included in the project pose more audit issues and greater code risks than a mature product.

Valuation

Toke’s current liquidity leverage is close to 3, indicating its market valuations are reasonably low.

Project Information

Business Introduction

Tokemak Operation Mechanism

Reactor:

A reactor is a specialized token pool for user-provided liquidity assets on Tokemak, which involves a Liquidity Provider and a liquidity director.

The following is an example of the Aave token reactor:

On the left are the Liquidity Providers (LP): LPs deposit a single asset into the token reactor and acquire corresponding tAssets to ensure a 1:1 ratio in exchange of the deposited asset upon exit. While assets in the reactor provide liquidity externally, non-TOKE token proceeds earned from the liquidity provision will be deposited directly into the Tokemak protocol and managed by the Tokemak DAO (composed of Toke holders). LPs only receive Toke rewards.

On the right are the Liquidity Directors (LD): Staked TOKE is used to control the whereabouts of liquid assets in the designated reactor. LDs stake their TOKE to a given reactor and use staking as a voting right to direct liquidity to the DEX of their choice.

Uniswap, Sushiswap, Balancer, and Deversifi are decentralized exchanges that will be directed by the reactor. LDs will also receive Toke rewards.

Reserve pool:

Each asset reactor creates a reserve pool of the corresponding tokenized asset (non-Toke tokens), which serves as the first layer of protection against impermanent loss. When an impermanent loss ocurs, it is first reimbursed through the reserve pool. Assets in the reserve pool are initially acquired through Decentralized Autonomous Organization (DAO) TO DAO, as will be further explained later.

If the decentralized exchange (DEX) is in an order book mode, the pricer role is also required.

Pricers:

Any non-automated market maker (AMM) requires real-time price data from a third-party institution. Tokemak leverages Pricers to set the buy and sell order prices.

Cycles:

Tokemak operates on epochs known as Cycles, which will initially be set to weekly (DAO may vote for changes later). Midway through the Cycle, assets can be deposited, and LD’s votes can be rearranged. Assets will be deployed when a new Cycle begins, and LPs get their assets back at the end of the Cycle if they request withdrawal mid-Cycle.

tAssets:

tAssets are tABC tokens that LPs receive when they deposit tokens into a Token reactor. These tABC tokens represent LPs’ underlying claim to the assets they deposited into the Token reactor, available to be redeemed 1:1 at any time (pending Cycle withdrawal period). tAssets are transferable, so whichever wallet holds the tABC tokens can claim the underlying assets deposited in the pool and receive rewards from the assets.

Automatically Optimize Liquidity Allocation

The Tokemak platform automatically offers a ‘balance’ between the supply and demand of LPs and LDs to an optimal level through a dynamic yield balancing mechanism, eliminating the need to determine each reactor’s incentive through the community.

The balance is shown as below:

Revenue Seesaw:

If a large amount of ABC tokens are deposited on the left side of the reactor, while LD stakes a small amount of TOKE on the right side, the annual percentage yield (APY) will increase on the LD side, thus stimulating the LD to stake more TOKE and direct that liquidity. Conversely, if a large amount of TOKE is staked on the right side whereas few ABC tokens are deposited, LP gains a higher APY to incentivize more tokenized assets to be deposited.

Redistribution of Proceeds:

Toke rewards are not redeemed from the actual mining rewards of a particular token pool, but are purely based on the supply and demand for that liquidity in the platform. Stepping outside the existing liquidity incentive model, this approach provides a secondary distribution of liquidity revenue within the platform through its revenue seesaw mechanism, making liquidity independent of the revenue incentive mechanism of second pool mining.

As an example, a project owner wants to increase the liquidity of its tokens, but the traditional incentive model forces the project owner to incentivize the LP by increasing the inflation, as its asset pair ABC/USDT produces low mining yield on a particular exchange. However, on Tokemak, the revenue seesaw will continue to attract LPs, provided that the project owner holds and stakes a certain amount of Toke on the right side of the ABC asset reactor. The project owner can also direct liquidity to its needs, and the more Toke it stakes, the more long-term LPs it will attract.

DAO TO DAO Mode

Before a new token reactor is built on Tokemak, token assets should be deposited into a reserve pool, where non-Toke tokens are initially swapped with Tokemak’s protocol token Toke.

The reserve pool acquires assets through DAO TO DAO communication, where both parties can exchange or lend each other the required tokens according to their respective needs for mutual benefit.

If the parties are on a lending basis, the lending will be decentralized through Rari Capital’s Fuse platform. Fuse is an interest rate borrow-lending protocol for DAO, which was launched in March this year and will not be detailed here. This DAO TO DAO model is more dependent on the community’s business development capabilities upfront. The Tokemak team has actively communicated with more than 20 DAOs, gaining rich resources and showing strong business capabilities.

Main Tokemak Users

- Liquidity Providers: LPs stake their idle assets to provide liquidity and receive a corresponding return.

- Liquidity Demanders (project owners and DEX): Liquidity Demanders acquire directing rights for sustainable liquidity by holding and staking Toke, and managing the liquidity of target tokens across multiple exchanges.

- Liquidity-directed speculators: They aim to share LD’s high returns in a reactor, rather than increasing the liquidity of a particular project.

Project Progress

Tokemak is still in the start-up phase and is planned to be initiated through a series of events called “Cycle Zero”, which consists of three steps as follows:

Step 1- DeGenesis: DeGenesis is an initial phase from July 27 to August 6, during which its whitelisted addresses receive their first TOKE release by submitting ETH and USDC. Tokemak ultimately raised $21.65 million through DeGenesis, with a final price of $8 for TOKE.

Step 2- Genesis Mining Pool: It is an additional pre-launch stage where users are allowed to mortgage single assets: ETH and USDC, while assets in the pool will be used to provide liquidity and obtain corresponding TOKE rewards. Even after ‘Cycle Zero’, the mining pool will remain competitively incentivized to accumulate necessary token pairs for liquidity deployment.

Step 3- Reactor mortgage events: Starting at the end of September (lasting 7 days), the first reactors will be selected from the candidate projects below. Then, toke holders will vote for five projects to create five reactors, and more will be created later.

The Tokemak team has already established contact with more than 20 DAOs. After voting for the five reactors to be built, the team will communicate with them via DAO TO DAO to obtain appropriate assets, and if it fails, it will continue to communicate with the sixth project, and so on.

Code audit: Tokemak has now passed the initial Bits audit and the Omniscia audit.

Tokemak Operations

Tokemak is in its early stage when detailed documentation has not yet been released, but with positive market responses, its Total Value Locked (TVL) continues to rise steadily, and it has surpassed Alpaca in market capitalization.

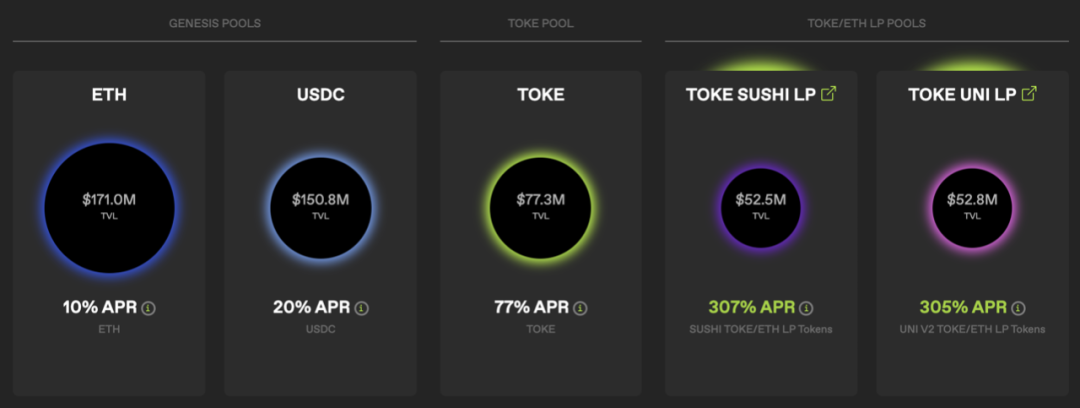

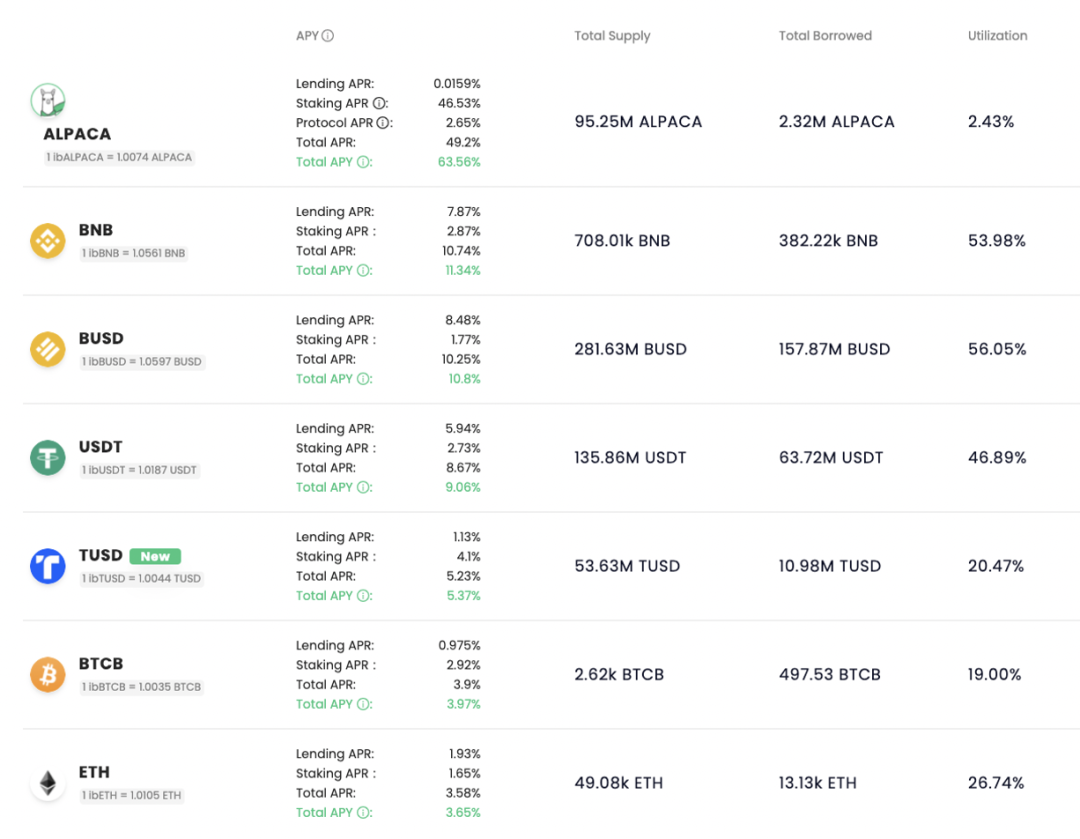

Currently, Tokemak is only open for Toke’s common and liquidity pools, with the main product (reactor) coming online soon. The yield of the mining pool is shown in the following chart:

The market is optimistic about Tokemak’s late performance.

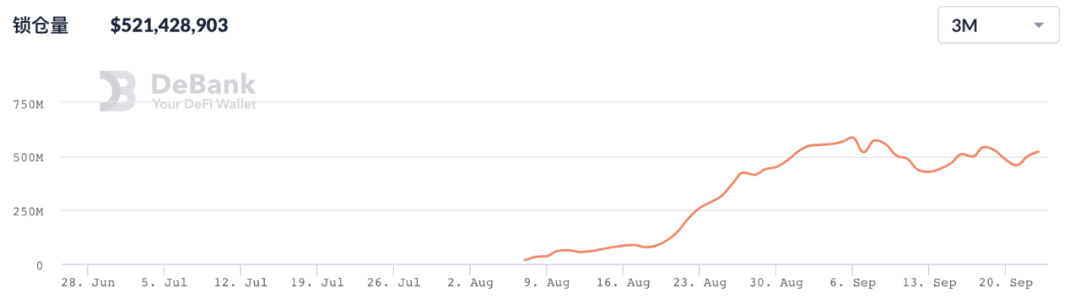

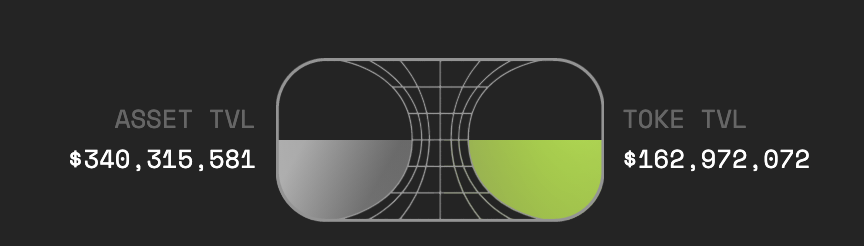

Tokemak has seen Toke price rise from $8 to $50 since the first Toke release, before it currently stabilizes near $35. Its TVL hovers around $500 million, of which $300 million is the value locked of non-Toke assets, ranking 18 among similar financial products in the defillama platform.

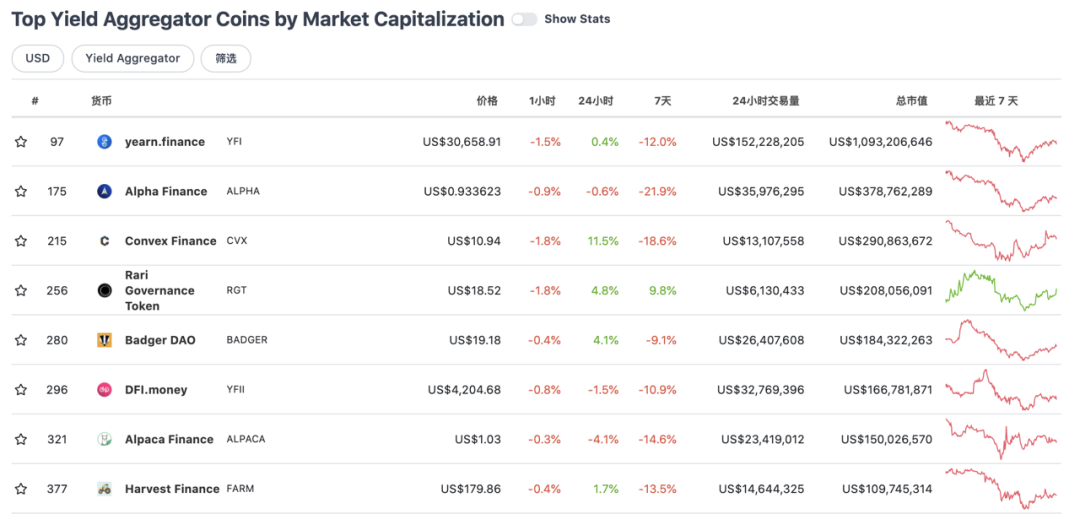

Toke now has a token circulation market cap of $160 million and a total Coingecko ranking of 310. It ranks seventh in the yield aggregator category and exceeds Alpaca Finance in current market capitalization.

It is important to note that Alpaca’s TVL reaches $1.3 billion, much higher than Tokemak’s $300 million, but this does not indicate Tokemak is overestimating. Due to the special token model, Tokemak’s token market capitalization is not suitable for horizontal comparison with other projects, and will be explained in detail in the Token Model section.

Team

Tokemak originally started as a project called “Fractal”, a market maker providing liquidity for DeFi, not a Fractal project on the Polkadot Chain, although more than one project is named Fractal.

Tokemak‘s core team members include:

- Carson Cook: Ph.D. in Physics, M.S. in Electrical Engineering, worked in FinTech at McKinsey, and has experience trading in the foreign exchange market. Since 2017, Carson has been involved in cryptocurrency trading. In early 2018, he founded Fractal, which had been running for more than three years as a DeFi market maker specializing in liquidity services for centralized exchanges before Tokemak was born out of this centralized market maker.

- Bruno: Previously worked for a Fortune 500 firm, where he was responsible for designing Tokemak’s Token-economy model.

- Craig: He has years of experience leading business development and marketing efforts for technology startups.

- Paul: Responsible for design and community work.

Financing

In April 2021, Tokemak closed a $4 million round of funding led by Framework Ventures with participation from Electric Capital, Coinbase Ventures, North Island Ventures, Delphi Ventures and ConsenSys.

Summary

Tokemak is a protocol for achieving sustainable DeFi liquidity, designed to address the difficulty, instability and high cost of accessing liquidity under existing liquidity incentive models.

Compared with existing revenue aggregators, Tokemak adopts a novel liquidity management system. Catering to both Liquidity Demanders and Liquidity Providers, it redistributes returns based on the supply and demand of liquidity within the platform to maximize the efficiency of liquidity allocation. Tokemak is expected to be the next-generation liquidity management infrastructure to help project owners better access and manage their token liquidity.

It has a veteran team with years of experience as a centralized market maker in the DeFi space, and an excellent financing lineup led by Framework Ventures.

Although the project is in its infancy stage, it is progressing steadily. The project has gone live with common and liquidity pools of its platform token Toke, with a value locked of $300 million (excluding the Toke value) and a TVL (including the Toke value) of about $500 million. By the end of September, it plans to launch the main product interface and open a liquidity directing pool of five project tokens. The team has already communicated with over 20 projects via DAO to DAO, and has received cooperation intention from some of them wanting Tokemak to help them better manage their token liquidity.

Therefore, Tokemak deserves continued attention as a new liquidity solution and management tool for project owners and DEX.

Business Analysis

Industry Space

Liquidity is critical to financial markets. An illiquid market is exposed to inefficient trading, easily manipulated market prices, and a broken price discovery mechanism, eventually entering an infinite loop.

A liquid market, on the other hand, has buyers and sellers at all times. If there are many buyers and sellers in a market, then it is called a deep market showing high liquidity, otherwise, the market is characterized by low liquidity and shallow market depth.

Early Liquidity Dilemma of Token Projects

In the early days, blockchain startups had to distribute a multitude of tokens via airdrop and single-token mining in order to promote their projects. As a result, a large number of project tokens were sold off when their value was not yet fully understood, but very few people were willing to provide liquidity for the project tokens. This made the tokens so illiquid that they cannot absorb selloff pressure in the market, and consequently their price and value often fell apart.

A project owner, for example, airdrops 100 thousand tokens, 50% of which will be sold unconditionally, 50% held for value, and only 5% used for liquidity mining. In the short term, 5% liquidity cannot take 50% of the tokens sold. Even if half of the participants recognize and think highly of the project, the lack of liquidity makes tokens’ market prices fall sharply and deviate from their normal market values, which will easily cause a vicious circle and seriously affect the healthy operation of the token ecology.

High subsidies attract liquidity. To avert that outcome, the project owner opts for both single-token staking mining and liquidity mining models, which are ultra-subsidized by way of inflation to minimize short-term selloff pressure while increasing the liquidity of tokens.

The highly subsidized approach is inefficient and costly. Through the subsidized approach, high subsidies do attract a large amount of short-term liquidity in the early stage, but slippage remains high for many token transactions, and most project owners fail to attract long-term LPs to provide sufficient liquidity for their project tokens. The short-term liquidity of a day or a week or two attracted by the highly subsidized approach does not make much sense, because once the yields drop later, the liquidity dries up immediately. Additionally, some teams choose to hire a centralized market maker at a high cost to help provide sufficient liquidity, although the cost is a significant expense for many startups.

In brief, traditional access to liquidity is a high-cost, low-return deal for many projects. Thus, Tokemak hopes to help these projects to access sustainable liquidity in a better way.

Tokemak Market Size Outlook

Open Up Long-tail TVL Market

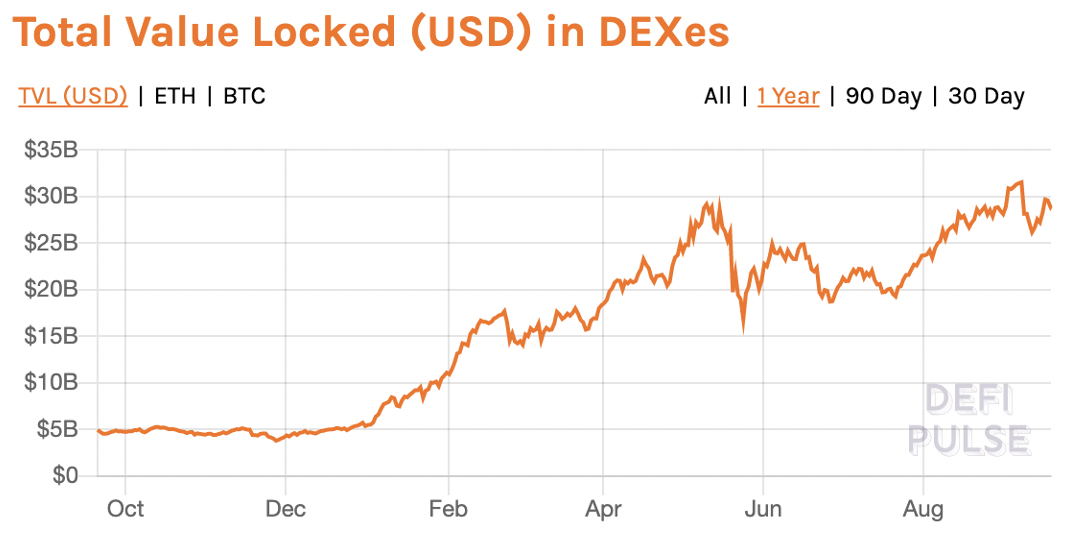

Currently, Defi’s TVL approximates $30 billion, or around $20 billion excluding stablecoin pairs. The Tokemak-backed Uniswap, Sushiswap, Balancer, and Deversifi exchanges have a TVL of around $12 billion. As the chart below shows, DEX’s TVL continues to grow steadily.

DEX’s TVL is dominated by trading pairs of ETH, wBTC, and stablecoins, followed by popular tokens, with a low TVL share for most long-tail assets. Taking UNI V2 as an example, ETH, wBTC and various stablecoin trading pairs statistically account for more than 30% of the TVL, the top 50 market-making asset pairs for over 60%, trading pairs ranked between 50 and 90 for about 20%, and the bottom 50% for less than 20%.

If Tokemak helps create better token liquidity for projects ranked after 50, this will bring significant incremental TVL to the current decentralized exchanges.

Tokemak’s current net TVL (excluding Toke value) totals $300 million, namely the values locked of ETH and USDC. By the time the main product is launched, matching liquid assets will flow further into Tokemak, and given a 50%-80% utilization of these assets, the TVL will grow to around $500-600 million.

Tokemak lock-in amount (9/27/2021)

Tokemak’s TVL would rise to $1.2 billion if it added 10% liquidity to the decentralized exchanges of intermediate and tail asset pools, in line with the current TVL of Alpaca (a leveraged mining project on the BSC chain), ranking 5th in its category at DeFillama. And a 30% increase in liquidity would bring the TVL to $2.4 billion, second only to YFI, ranking 3rd in its category.

Competition Landscape

Prior to the analysis on the competitive relationship between Tokemak and similar programs, it is important to understand the hidden borrowing and lending relationship in Tokemak mechanism.

Tokemak’s LP transfer its impermanence loss risk to LD, and hosts its liquidity to the platform protocol for targeted use by LD. This means that LP lends its assets to LD and receives corresponding lending proceeds.

Unlike over-collateralized lending models like AAVE, Tokemak lends leveraged assets. To be specific, AAVE has no control over the assets lent through its platform and can only secure the assets by over-collateralizing them, leading to a capital utilization rate of less than 50% or even less. Tokemak, on the other hand, cleverly uses smart contracts to connect liquidity making and lending operations. With the protocol to provide safe custody for the assets, it only transfers usage rights, without the need for staking. This greatly increases the efficiency of capital utilization. Therefore, it is possible to direct the liquidity of multiple Toke assets with 1 Toke.

Leveraged mining platforms are in this respect the same as Tokemak, with their users partially overlapping. Take Alpaca Finance as an example for comparative analysis.

Competitive Advantages

Competition with Alpaca

Both Tokemak and Alpaca have lending pools with allocated assets such as ETH/USDT/DAI, where they compete with each other.

The following figure illustrates the yield and utilization rate of Alpaca’s single-currency loan:

Alpaca’s paired single-currency assets will be automatically matched as market making pairs and deposited in the exchange for higher returns. BUSD and BNB, the most utilized assets on Alpaca (around 50%), enjoy lending yields of around 10%.

The yields of paired asset pools depend on the asset end-return, asset utilization and how the return is distributed. In the long run (disregarding the incentives of short-term platform tokens), both Alpaca and Tokemak get asset end-returns from liquid market-making, and therefore their comprehensive rates of return are close, but primarily differ in the effective utilization of paired assets and the revenue distribution mechanism.

What advantages and differences does Tokemak have that can improve the utilization of its platform assets and the efficiency of revenue distribution?

Tokemak’s Advantages

Single Assets Provide Liquidity

LP on Tokemak is providing single-sided assets.

In pre-project developments, startup teams carry copious tokens, but are not willing to sell them in bulk, leaving a large amount of single-sided token assets on Tokemak. Then, the project owners may make good use of these assets to provide sufficient liquidity for their projects.

Other token holders, without the need to match asset pairs, simply provide idle unilateral assets to share in the benefits of liquidity provision.

Transfer the Risk of Impermanence Loss

Tokemak transfers the risk of impermanent loss that LP may face to LD.

When an impermanent loss occurs, Tokemak’s reactor reserve pool provides the first layer of protection to LP, and then rewarded Toke and staked Toke from LD in the reactor act as the second layer of protection.

In essence, LPs on Tokemak simply lend their idle assets to LDs through the Tokemak protocol. Compared with lending platforms like AAVE, Tokemak enables LDs to borrow money without over staking or liquidation risk, but offers a profitable leverage ratio.

Without considering contractual risks, it would be better for LPs to lend their liquid assets to a platform like AAVE than to Tokemak, because the return on liquidity provision is usually higher than that on inefficient lending.

tToke

All of Tokemak’s staked assets will receive corresponding tToke tokens, which are liquid and will have greater liquidity and more portfolios in the future, similar to ytoken on Yearn Finance.

Pool Liquidity Across Exchanges

Tokemak can pool liquidity from multiple exchanges, making it very convenient for project owners to manage the liquidity of their tokens across multiple exchanges.

Provide Sustainable Liquidity Without Mining, Selling, Withdrawal and Selloff Pressure

Tokemak pools together all token rewards earned for liquidity services and deposits them in its DAO reserve pool. The Tokemak protocol does not sell off these non-Toke assets in the absence of a large impermanent loss. These assets will serve as the underlying assets that underpin the value of Toke and provide ongoing liquidity services to the market.

The traditional approach of incentivizing liquidity mining by way of inflation provides liquidity to the market while adding more selloff pressure from mining, selling, and withdrawal. Furthermore, this short-lived incentive does not make much sense, as a significant contraction in liquidity will ensue from a rapid decline in liquidity mining incentives.

Seesaw Dynamic Rate-of-Return Mechanism to Better Distribute Revenue and Manage Liquidity

When the liquidity demander adjusts its staked Toke volume on Tokemak to its liquidity demand, the yield will dynamically change with the difference between supply and demand so that the liquidity supply and demand will be automatically modulated to an optimal equilibrium point. As one of Tokemak’s main innovations, this feature is not available in other liquidity projects in the current market.

Tokemak’s Differentiated Service Objects

LP:

Those who prefer low risks: any user can deposit a single-sided asset into Tokemak to offer liquidity and not have to bear impermanent losses (except for extreme risks). Tokemak is similar to AAVE or Alpaca, whereby users lend their assets to the protocol and receive interest.

LD:

- DAO: DAO leverages Tokemak’s liquidity to enhance and direct the liquidity of their projects as an alternative to the traditional liquidity mining model.

- New project: The new project can build its own token reactor at low cost, and the reactor may generate healthy liquidity for the project in a cost-effective manner through Tokemak.

- DEX: DEX leverages Tokemak to strengthen its market depth.

In the long run, Tokemak’s service targets are not the liquidity miners who are allured by high returns, but low-risk seekers who are willing to hold some token assets. Actually, these users are not willing to bear impermanent loss from market making and therefore leave their assets idle on hand, but Tokemak effectively helps them put their idle assets to use.

In addition, more important targets are the to b side, and DAOs, new projects or DEX that need liquidity, whose original liquidity access is too costly and unsustainable, but Tokemak can effectively reduce their liquidity access costs and provide them with more stable liquidity.

Summary

Tokemak is grounded in helping Liquidity Demanders better manage and direct their liquidity, rather than maximizing the revenue of miners. Its mechanism is significantly different from most existing liquidity mining aggregation platforms.

Tokemak is a novel decentralized liquidity management tool and solution featuring multiple original designs to enable low-risk market making, continuous liquidity access, liquidity management, see-saw dynamic yields and more.

Token Model Analysis

Token Distribution

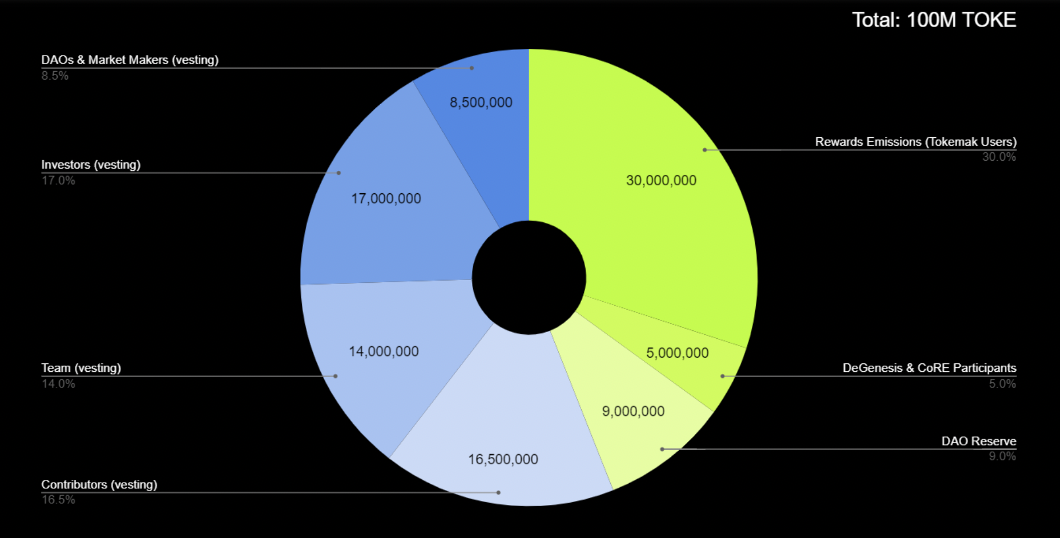

Tokemak’s protocol token, TOKE, with a total supply of 100 million, is allocated as follows:

- Total supply: 100,000,000 TOKE

- 30,000,000 TOKE (30%): Reward release (24 months)

- 5,000,000 TOKE (5%): TOKE will be released for the first time in case of the DeGenesis event and CoRE (Reactor Mortgage Event) during Cycle Zero

- 9,000,000 TOKE (9%): DAO reserves, which are available for swap of non-Toke assets in DAO TO DAO communications.

- 16,500,000 TOKE (16.5%): Contributor (12-month cliff + 12-month linear release)

- 14,000,000 TOKE (14%): Team (12-month cliff + 12-month linear release)

- 17,000,000 TOKE (17%): Investor (12-month cliff + 12-month linear release)

- 8,500,000 TOKE (8.5%): DAOs & Market Makers (12-month cliff + 12-month linear release)

It is worth noting that the proportion of Toke rewards being released is lower than that in other projects, and conversely, teams, investors, and contributors are highly aggregated, accounting for nearly 50%. The value of Toke tokens comprises the right to govern Tokemak DAO and the right to distribute liquidity.

Token Value Capture

The value of Toke tokens comprises the right to govern Tokemak DAO and the right to distribute liquidity.

Governance

Toke holders are given the right to govern Tokemak DAO and have the Tokemak protocol revenues at their disposal through DAO.

Tokemak DAO governance includes controlling protocol fee allocation, calibrating cycle length, adding new token reactors, and modifying protocol security measures (reserve/deployment ratio + TOKE mortgage parameters).

Tokemak Agreement Revenues are Cumulative:

While most platform tokens realize their values by charging fees for their services (transaction fees, revenue sharing, etc.), the Toke token captures all the revenues earned by the platform for providing liquidity.

Tokemak will only pay TOKE rewards to LPs and LDs and retain all non-Toke assets gained from external liquidity provision through the protocol. This indicates that Tokenmak will accumulate market making proceeds, depositing them as the protocol’s pending profits as well as risk reserves. As the size of the proceeds expands, the underlying assets will slowly aggregate and increase the intrinsic value of Toke.

Singular Point:

Tokemak keeps pooling non-Toke assets to a point where its liquidity becomes self-sufficient and reaches a certain singularity. Afterwards, Tokemak does not need third-party LPs, nor does it continue to unleash its TOKE rewards, as TOKE holders will then decide how to use these asset reserves to provide liquidity.

Liquidity Distribution Right

Toke holders possess the right to allocate liquidity of all platform assets in the protocol. Any user who wants to access liquidity through Tokemak should hold and stake Toke in order to attain the liquidity allocation right.

Benefits and Risks

Toke tokens capture the value of all Tokemak liquidity with the attendant risks.

When an impermanent loss occurs, Tokemak’s reactor reserve pool provides the first layer of protection to LP, and then rewarded Toke and staked Toke from LD in the reactor act as the second layer of protection. Unlike the independent clearing mechanisms of other aggregators, the Tokemak protocol allows the Toke reserve pool to be sacrificed first in the event of significant market volatility, which amounts to a dilution of Toke assets and is essentially an insurance policy that everyone buys together.

The protocol maximizes the amount of assets that LPs can get back, but subjects Toke to more fluctuations in value.

Five Core Questions

What Business Cycle is the Project in? Is It in Maturity or the Early to Mid-stage?

Tokemak is in its early days and faces many uncertainties. In terms of business model, the liquidity management market shows pockets of growth, a high business ceiling and strong sustainability. However, Tokemak has not yet launched its main product and white paper, with many details to be revealed, so it remains to be verified whether the project owner will launch the product as originally scheduled, whether the code will run smoothly and safely, and whether the business model will run through.

Does the Project Have a Solid Competitive Advantage? Where Does This Advantage Come From?

Tokemak is innovative: as a new-generation liquidity solution, it showcases many highlights and advantages. It stands on the side of Liquidity Demanders in response to current drawbacks of liquidity management, hence no direct counterparts.

Excellent financing background: The project is funded by a Framework Ventures-led group of well-resourced excellent investors in the DeFi space, including Coinbase, Delphi Ventures and ConsenSys.

The team background tallies well with the business direction: the team is experienced in the current project business as it had been involved in centralized market making for DeFi before, exactly the same as the business direction.

Is the Investment Logic of the Project Clear in the Medium to Long Term? Is It in Line with the General Trend of the Industry?

Liquidity management infrastructure is critical in the DeFi space in line with the general trend. But it is an issue to be addressed due to its novel business model that is not yet validated in the market, so it is unlikely to determine its long-term investment value at this time.

What are the Main Operational Variables of the Project? Are Such Variables Easy to Quantify and Measure?

In the first days, Tokemak attracted sufficient Liquidity Demanders based on the community’s operational capability. Currently, its community is well equipped with business resources and professional experience as shown by its community operations.

In the mid- to late stage, Tokemak will rely heavily on the virtuous cycle of the protocol, and will be much less dependent on community operations.

What is the Management and Governance Approach to the Project? How is Their DAO?

Tokemak has a high percentage of tokens held by the founding team, investors and contributors, and the team shows a strong control over the project. In the short to medium term, the project is likely to be operated and managed by the team.

But in the long run, Tokemak will be run through Tokemak DAO, composed of Toke holders.

Valuation

Valuing new token models is not an easy task. The token value model unique to Tokemak does not allow for side-by-side valuation comparisons with similar projects. Here, Toke is therefore valued using one of the simplest but most intuitive metrics — liquidity access leverage.

Liquidity Access Leverage = TVL of Staked Toke / TVL of Liquid Assets

Liquidity Access Leverage indicates how many times LD can control liquidity for every Toke owned. The higher the leverage, the higher the value of the Toke and the more conservative its valuation, and vice versa.

Toke value is the sum of the platform’s sustainable liquidity access value and the corresponding impermanent loss premium. The asset itself has 1x liquidity, and Tokemak leverage is currently in the 2-3x range. Then, considering the risk premium, a 3x leverage ratio is anchored for a conservative and reasonable valuation of Toke.

Toke value is estimated using the following parameter assumptions:

- 3x leverage ratio

- 50% initial capital utilization of non-Toke asset TVL

- 80% Toke staking participation

- Release 1,250,000 Toke every month in the first year

Tokemak TVL refers to the TVL of LP’s assets, excluding the value of Toke. The initial value of Tokemak TVL is calculated at 50% initial capital utilization rate:

Initial value of Tokemak TVL = non-Toke asset TVL ($360 million) * (1+0.5)

Toke price (estimated) = Tokemak TVL (non-Toke assets) / Toke leverage / Toke volume

Valuation in the context of slow TVL growth:

Note: Toke’s TVL is not part of Tokemak’s TVL

While the TVL of non-Toke assets grows at a rate of 20% per month (close to the rate of Toke inflation), the estimate of Toke price reasonably stabilizes around $50 in the early stage.

Valuation in the context of fast TVL growth:

Note: Toke’s TVL is not part of Tokemak’s TVL

Toke’s valuation steadily increases in the case of rapid growth, where TVL grows faster than Toke’s outstanding market capitalization.

The token reward yield of the protocol is inferred backwards by the above valuation logic.

Average annualized rate of return = Number of monthly Toke rewards * Toke price / (Tokemak TVL + market value of staked Toke) * 12

Based on the formula, the protocol releases 1.25 million Toke per month in the first year, all of which are used for platform incentives. Hence, the average annualized rate of return changes as below:

The measurements show that Tokemak brings a good revenue incentive to the platform through token inflation in the early stage. However, tokens used for rewards have a smaller share as more tokens are released, hence a diminishing incentive effect at the margin, which may put some pressure on the future growth of TVL.

In the medium to long term, token dilution will work little, and the incentive returns will gradually converge to the market average. It remains to be seen whether Tokemak can grow into a self-growing liquidity management platform.

*The valuation model is for reference only, as Toke price is highly sensitive to both Toke staking and leverage ratios.

Risks

Mechanism Risk

- Extreme bull and bear markets cause great impermanent losses, and subsequently severe Toke loss, which gives more downward pressure on Toke prices.

- For the liquidity demander, the value of leverage from Toke is paramount. When the TVL in the pool falls sharply, the leverage value also falls, which, coupled with the impermanent loss risk to the protocol, can create a death spiral.

- Since the Tokemak product is not yet live or detailed, it remains unknown how much demand there will be, and whether it will attract enough idle assets.

Smart Contract Risk

- Tokemak is a brand new project with a lot of original code, so it will take time to verify whether it will run smoothly and be able to resist hacking.

Operational Risk

- Tokemak involves frequent DAO TO DAO communications, hence a greater binding relationship between its initial development and the professional proficiency of DAO.

References

Carson Cook: Tokemak Is The Decentralized Liquidity Engine for DeFi

C.o.R.E. – Collateralization of Reactors Event

https://medium.com/tokemak/c-o-r-e-collateralization-of-reactors-event-2a2d5b2f8e70

Introducing: Tokemak | The Utility for Sustainable Liquidity

https://medium.com/tokemak/introducing-tokemak-the-utility-for-sustainable-liquidity-8b99a4757301

TOKEnomics:https://medium.com/tokemak/tokenomics-4b3857badc73

Tokemak in a five-minute nutshell: How to direct liquidity in a decentralized way?

What is Tokemak?